TL;DR:

- Effective fintech workflow optimization involves strategic process redesign, not just automation.

- Integrating AI, blockchain, and hybrid cloud-edge architectures enhances speed, compliance, and risk management.

- Prioritizing high-value workflows and measuring KPIs drives continuous improvement and return on investment.

Fintech workflow optimization is widely misunderstood. Most teams treat it as a synonym for automation, deploying bots to handle repetitive tasks and calling the project complete. But the real opportunity is far broader. Fintech improves NIM, reduces credit risk, and reshapes how organizations manage compliance, fraud detection, and customer experience simultaneously. The companies pulling ahead in 2026 are not simply automating existing processes. They are redesigning those processes from the ground up, integrating AI, blockchain, and cloud-edge architectures into a coherent operational strategy. This article breaks down exactly how to do that, and what to watch out for along the way.

Key Takeaways

| Point | Details |

|---|---|

| Holistic optimization | True workflow improvement blends automation, process redesign, and strategic technology for maximum impact. |

| Cloud vs edge tradeoff | Cloud gives scale and ML power, while edge is fastest for real-time compliance—and the best solutions mix both. |

| Legacy integration hurdles | Connecting old systems to new workflows requires technical and compliance expertise, plus careful human oversight. |

| Specialized AI wins | Specialized machine learning delivers up to 93% accuracy—a smart investment compared to general AI in fintech. |

| Value over risk | The highest ROI comes from optimizing for business impact, not just risk reduction or compliance wins. |

Defining fintech workflow optimization: From automation to strategic integration

Workflow optimization in fintech is not a single technology or a one-time project. It is a continuous discipline that combines process reengineering, system integration, and targeted automation to improve speed, accuracy, and compliance across financial operations. The distinction matters because many organizations invest heavily in point solutions, only to find that isolated automation creates new bottlenecks rather than eliminating old ones.

At its core, fintech workflow optimization asks a harder question than “what can we automate?” It asks: “Which processes, if redesigned entirely, would generate the most measurable value?” That reframe shifts the conversation from tooling to strategy.

Consider AI-driven financial transaction processing as a practical example. A team that simply automates manual entry has saved some labor. A team that redesigns the entire transaction pipeline, incorporating real-time validation, anomaly detection, and automated reconciliation, has fundamentally changed its risk profile and throughput capacity. The latter approach is what allows organizations to boost transaction efficiency at scale without proportionally increasing operational overhead.

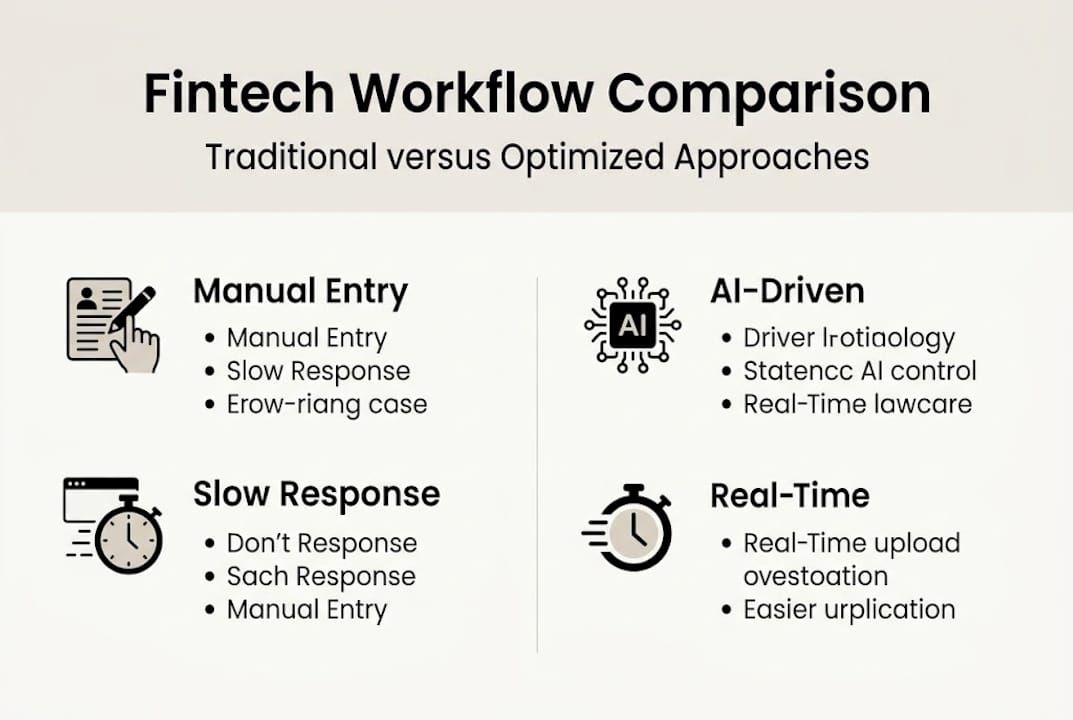

The table below illustrates the contrast between traditional and optimized workflows across key dimensions:

| Dimension | Traditional workflow | Optimized workflow |

|---|---|---|

| Processing speed | Batch, delayed | Real-time or near-real-time |

| Error rate | High (manual steps) | Low (automated validation) |

| Compliance handling | Reactive | Proactive, embedded |

| Scalability | Limited by headcount | Scales with infrastructure |

| Risk exposure | Operational and credit | Cyber and vendor risk |

One common misconception is that optimization eliminates risk entirely. In reality, fintech reduces bank risks via efficiency but introduces new ones, particularly in cybersecurity and operational resilience. Recognizing this trade-off is essential for teams that want to pursue faster workflow ROI without creating blind spots in their risk architecture.

Key areas where strategic integration outperforms simple automation include:

- End-to-end process visibility across payment, lending, and compliance workflows

- Interoperability between legacy systems and modern APIs

- Embedded compliance logic that adapts to regulatory changes automatically

- Modular architecture that allows components to be upgraded independently

The goal is not to automate chaos faster. It is to redesign workflows so that speed and control reinforce each other.

Core technologies powering workflow optimization in fintech

With a clear definition in mind, we can now explore the technologies that underpin efficient fintech workflows. No single platform handles everything well, and understanding where each technology excels prevents costly misalignment between tools and use cases.

Automation platforms form the operational backbone. They handle rule-based tasks, orchestrate multi-step processes, and connect disparate systems through pre-built connectors. The best platforms today go beyond simple robotic process automation, offering event-driven triggers, conditional logic, and audit trails that satisfy regulatory requirements.

AI and machine learning modules add adaptive intelligence. Where automation follows rules, AI learns from patterns. This distinction is critical for use cases like AI in fraud prevention, where the threat landscape evolves faster than any static ruleset can track. An AI workflow assistant can flag anomalies, prioritize alerts, and reduce false positives without requiring constant manual reconfiguration.

The cloud versus edge decision deserves careful analysis:

| Criteria | Cloud computing | Edge computing |

|---|---|---|

| Latency | Higher | Lower |

| Scalability | Excellent | Limited |

| ML complexity | Superior | Moderate |

| Real-time processing | Adequate | Superior |

| Regulatory sensitivity | Requires controls | Easier to isolate |

Cloud excels for complex ML, while edge is superior for real-time processing but can be less scalable. For fintech teams managing both high-frequency transactions and complex risk models, neither option alone is sufficient.

The numbered steps for evaluating your technology stack:

- Map latency requirements for each workflow category

- Identify which processes involve sensitive regulatory data

- Assess current ML model complexity and training frequency

- Determine scalability requirements over a 24-month horizon

- Select a hybrid architecture that assigns workloads to the appropriate layer

Blockchain integration adds a dimension that neither cloud nor edge alone can provide: immutable audit trails and trustless transaction verification. For cross-border payments and settlement workflows, secure workflows with blockchain reduces reconciliation time and counterparty risk simultaneously.

Pro Tip: Combine edge computing for real-time transaction validation with cloud infrastructure for model training and compliance reporting. This hybrid approach lets teams meet latency requirements without sacrificing the analytical depth that complex ML models demand.

Addressing complexity: Legacy systems, compliance, and human oversight

Technology alone can’t solve everything. Complexity often comes from legacy dependencies, compliance requirements, and operational risks that no single platform resolves out of the box.

Legacy system integration is consistently the most underestimated challenge. Older core banking systems were not designed for API-first architectures, and retrofitting them requires careful abstraction layers, data mapping, and extensive testing. Legacy system integration challenges also drive up the evaluation costs for advanced AI, because models must be validated against data formats and business logic that predate modern standards.

Regulatory compliance adds another layer of complexity. KYC and AML requirements are not static. They evolve with geopolitical shifts, new financial crime typologies, and updated guidance from regulators. Automated compliance solutions can embed rule updates directly into workflow logic, but they still require human oversight to handle edge cases and regulatory interpretation.

Deepfake risk in identity verification is an emerging threat that many optimization projects overlook. As synthetic media technology improves, traditional document and biometric checks become less reliable. Teams building or upgrading identity verification workflows need to account for this explicitly, not treat it as a future problem.

“The evaluation costs for agentic AI in finance are not trivial. Organizations that skip rigorous testing in favor of speed often discover that their AI systems behave unpredictably under real-world conditions, creating compliance exposure that far exceeds the cost of proper evaluation.”

Key barriers and practical solutions:

- Legacy integration debt: Use middleware abstraction layers to decouple modern workflows from legacy core systems

- KYC/AML compliance drift: Implement automated rule versioning so compliance logic updates without manual intervention

- Deepfake IDV risk: Layer liveness detection and behavioral biometrics alongside document verification

- Agentic AI unpredictability: Maintain human-in-the-loop checkpoints for high-stakes decisions

- Siloed priorities: Align IT, compliance, and operations teams around shared workflow KPIs

For teams managing financial processing at scale, a structured IT leader’s guide to system architecture helps frame these trade-offs in terms that both technical and executive stakeholders can act on. The cost savings in automation are real, but only when complexity is addressed systematically rather than deferred.

Measuring ROI and success: Practical steps for implementing workflow optimization

With these challenges in mind, let’s turn to actionable strategies for successful workflow optimization and how to measure its impact. The most common failure mode is not poor technology selection. It is poor measurement. Teams that cannot quantify the before-and-after state of a workflow cannot demonstrate value, cannot secure continued investment, and cannot identify where to improve next.

The implementation process for scalable process solutions follows a repeatable structure:

- Needs analysis: Map current workflows, identify bottlenecks, and quantify their cost in time, error rate, and compliance exposure

- Prioritization: Rank workflows by value potential, not just risk reduction. High-volume, high-complexity processes yield the greatest returns

- Technology selection: Match tools to specific workflow requirements rather than adopting platforms wholesale

- Pilot implementation: Deploy in a controlled environment with defined success metrics before scaling

- Measurement and iteration: Track KPIs continuously, adjust configuration based on real performance data, and expand incrementally

KPIs worth tracking include transaction processing time, error rate per thousand transactions, compliance exception frequency, and cost per processed workflow unit. These metrics create a feedback loop that drives continuous improvement rather than one-time optimization.

The data on model selection reinforces the importance of targeted solutions. General LLMs achieve 66% accuracy versus specialized ML at 93% in accounting tasks, which means that deploying a general-purpose AI model in a domain-specific financial workflow is not just suboptimal. It is measurably costly.

Pro Tip: For high-value processes like loan underwriting or fraud adjudication, resist the temptation to use general-purpose AI because it is easier to deploy. The ROI gap between a general model and a specialized one is significant enough to justify the additional configuration effort. Teams that follow enterprise automation best practices consistently report better outcomes when they match model specificity to process complexity.

What most guides miss: Why value beats risk avoidance in fintech workflow optimization

Most workflow optimization guides frame success primarily as risk reduction. Fewer errors, fewer compliance violations, fewer manual touchpoints. That framing is not wrong, but it is incomplete, and it leads organizations to optimize defensively rather than competitively.

The fintech teams that consistently outperform their peers are not the ones with the lowest error rates. They are the ones that have used workflow optimization to create measurable customer value, whether through faster loan decisions, real-time payment confirmation, or personalized financial products delivered at scale. Fintech’s complexity trade-offs are real, but they are worth navigating when the value creation opportunity is clear.

Risk avoidance is a floor, not a ceiling. Organizations that treat compliance and error reduction as the primary goal tend to under-invest in the workflow improvements that drive revenue and retention. High-performing teams use workflow automation perspective to align optimization efforts with business outcomes, not just audit findings.

The practical implication: when prioritizing which workflows to optimize next, weight the value creation potential alongside the risk reduction benefit. A workflow that reduces fraud exposure by 10% but adds no customer value is a lower priority than one that cuts loan processing time in half while also reducing manual errors. Both matter. Value should lead.

Explore tailored fintech solutions for scalable workflow optimization

Having explored the actionable steps and perspective, here is how you can leverage powerful solutions to advance your own fintech workflow optimization. Bitecode.tech offers modular, pre-built components that let fintech teams deploy production-ready systems with up to 60% of the baseline already built, dramatically reducing time-to-value.

Whether your priority is deploying workflow automation solutions that handle complex financial processing, building customer-facing systems with custom CRM modules, or integrating a blockchain payment system for secure, auditable transactions, the platform provides the modular foundation your team needs to move fast without accumulating technical debt. Explore the full range of solutions and find the components that match your workflow priorities.

Frequently asked questions

How does fintech workflow optimization improve financial processing efficiency?

By automating tasks and integrating specialized AI, companies can process transactions faster and reduce manual errors significantly, with some implementations achieving up to 40% throughput gains.

What are the biggest challenges when integrating legacy systems in fintech workflow optimization?

Legacy system integration creates technical complexity, increases evaluation costs for advanced AI, and can slow optimization efforts. Integration challenges often require middleware abstraction layers to bridge old and new architectures effectively.

How do fintech companies balance compliance and workflow speed?

Optimized workflows use automation and human oversight to handle KYC/AML checks without sacrificing processing speed. Hybrid automation and oversight models embed compliance logic directly into workflow steps, reducing manual review bottlenecks.

Is edge computing better than cloud for real-time fintech operations?

Edge computing offers lower latency and is ideal for real-time tasks, while cloud is more scalable but carries higher latency and cost. Most production environments benefit from a hybrid approach that assigns workloads to the appropriate layer.

What’s the ROI of using specialized AI versus general LLMs in fintech accounting?

Specialized ML achieves 93% accuracy versus 66% for general large language models in accounting tasks, yielding a substantially higher ROI for domain-specific financial workflows.