TL;DR:

- Automation in finance yields 60-80% time savings and 75% cost reduction on invoices.

- Core technologies include RPA, AI, OCR, and machine learning, each suited for specific tasks.

- Successful automation requires starting with high-volume, rule-based processes and building hybrid workflows.

Finance teams that dismiss automation as hype may be leaving serious money on the table. Independent benchmarks show 60-80% time savings and a 75% reduction in invoice processing costs for organizations that have moved past pilot programs into scaled deployment. These aren’t aspirational projections from vendors — they’re measurable outcomes from enterprises running automation across accounts payable, reconciliation, and reporting workflows. This article walks finance executives through the core technologies driving these results, the real ROI numbers behind them, the limitations that demand honest planning, and a practical framework for building automation programs that actually scale.

Key Takeaways

| Point | Details |

|---|---|

| Automation delivers measurable impact | Enterprises see 60–80% time savings and significant cost reduction through finance automation. |

| Start with high-volume processes | Launching automation in areas like AP/AR ensures fast ROI and smoother scaling. |

| Hybrid approach is key | Organizations achieve the best results by combining automation with strategic human oversight. |

| Track KPIs for success | Measuring cost per invoice, cycle times, and error rates helps maximize automation value. |

| Full AI autonomy is unrealistic | Human expertise remains essential for exceptions, data nuances, and regulatory compliance. |

Understanding automation technologies in finance

With a sense of the dramatic benefits established, let’s break down what automation technologies actually do and where they add the most value in financial operations.

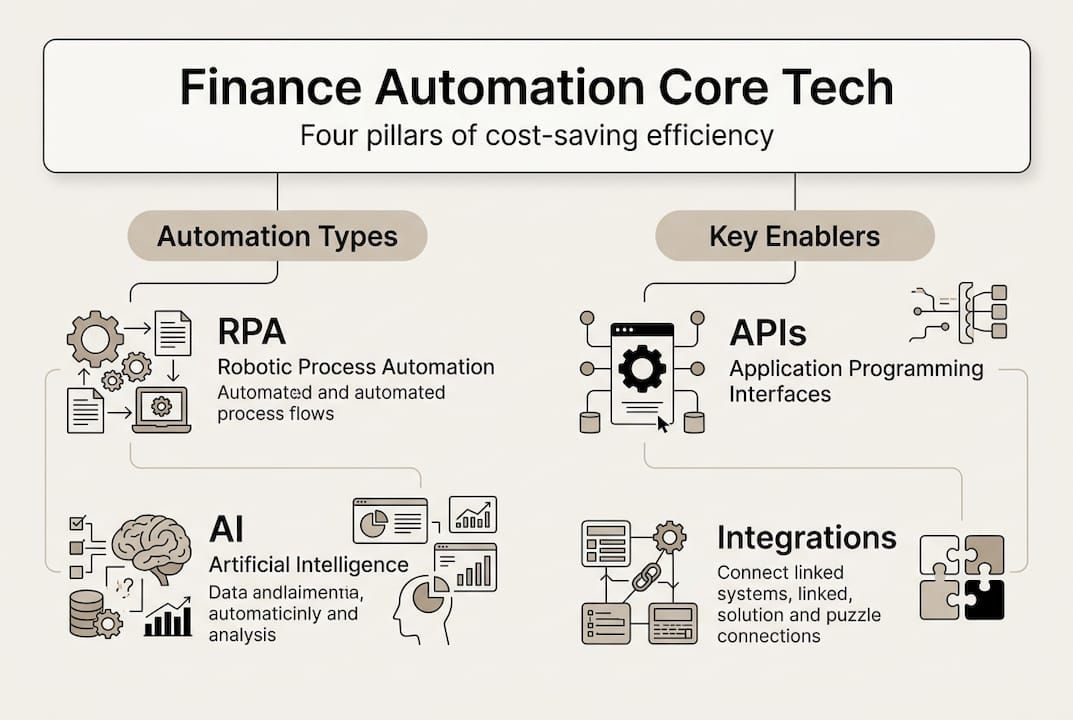

Four core technologies power modern finance automation: Robotic Process Automation (RPA), Artificial Intelligence (AI), Optical Character Recognition (OCR), and machine learning. Each plays a distinct role, and understanding those roles prevents organizations from deploying the wrong tool for the wrong problem. RPA, AI, OCR, and machine learning are now standard in accounts payable, accounts receivable, reconciliation, reporting, and forecasting workflows across mid-market and enterprise finance teams.

| Technology | Primary function | Best-fit finance tasks |

|---|---|---|

| RPA | Mimics repetitive human actions in software | Invoice entry, payment runs, data transfers |

| AI | Pattern recognition and decision support | Fraud detection, anomaly flagging, forecasting |

| OCR | Converts documents to structured data | Invoice capture, contract extraction, statement parsing |

| Machine learning | Learns from historical data to improve predictions | Cash flow modeling, credit risk scoring, variance analysis |

RPA handles the mechanical layer: logging into systems, copying data between platforms, triggering payment approvals. It doesn’t think — it executes. That’s precisely its strength for high-volume, rule-based tasks where human error is costly and speed matters.

AI and machine learning operate at a higher level. They analyze patterns across thousands of transactions, flag exceptions that don’t fit historical norms, and generate forecasts that would take analysts days to produce manually. Pair these with a solid finance automation guide and teams can build a layered system where each technology handles what it does best.

OCR is the often-underestimated bridge between paper-based or PDF workflows and structured digital data. Without it, even the most sophisticated RPA or AI layer still requires manual data entry at the front end, which defeats the purpose.

Key areas where these technologies combine effectively:

- Accounts payable: OCR captures invoice data, RPA routes it for approval, AI flags duplicates or anomalies

- Accounts receivable: Machine learning predicts payment timing, RPA sends reminders and posts receipts

- Reconciliation: RPA matches transactions across systems; AI escalates unmatched items for human review

- Reporting: AI aggregates data and generates draft reports; humans review and interpret

Integration with ERP systems is where these tools reach their full potential. Standalone automation that doesn’t connect to your core financial system creates data silos rather than eliminating them. Effective AI transaction monitoring depends on clean, connected data flows across the entire financial stack.

Measuring ROI: Real-world impact and benchmarks

Armed with knowledge of the tools, executives next want proof: how do these approaches translate to measurable ROI?

The numbers are more compelling than most finance leaders expect. 60-80% time savings, 75% cost per invoice reduction, and 111-287% ROI are documented benchmarks for finance automation programs — not outliers, but ranges observed across multiple enterprise deployments tracked in Forrester’s Total Economic Impact studies.

| Metric | Pre-automation baseline | Post-automation result |

|---|---|---|

| Invoice processing cost | $12-15 per invoice | $3-4 per invoice |

| Invoice processing time | 10-14 days | 2-3 days |

| Reconciliation time | 5-7 days monthly close | 1-2 days monthly close |

| Error rate (AP) | 3-5% | Under 1% |

| ROI (3-year) | N/A | 111-287% |

The payback period for accounts payable pilots typically runs 4 to 7 months. That’s a short runway for a technology investment in the enterprise context, and it explains why AP is almost always the recommended entry point for organizations new to finance automation.

KPIs worth tracking from day one of any automation program:

- Cost per transaction (before and after automation)

- Processing cycle time (end-to-end, not just touchpoints)

- Exception rate (how often automated processes require human intervention)

- Straight-through processing rate (percentage of transactions completed without manual handling)

- Employee hours redirected to higher-value work

- Error rate and rework frequency

The software selection checklist matters here because the KPIs you can actually measure depend heavily on whether your automation platform exposes the right reporting hooks. Organizations that skip this step often find themselves unable to demonstrate ROI to the board, even when the operational improvements are real.

One insight that surprises many executives: the efficiency gains compound. Faster invoice processing improves cash flow visibility, which improves forecasting accuracy, which improves working capital decisions. The processing systems guide for IT leaders reinforces this point — automation ROI isn’t just a cost story, it’s a data quality and decision-making story.

Edge cases and limitations: Navigating the challenges

While the ROI is compelling, real-world implementation faces hurdles that demand strategic solutions.

No honest assessment of finance automation skips the hard part. Edge cases include non-standard data, exceptions, regulatory hurdles, and skills gaps — and full AI autonomy remains out of reach in finance because the domain requires contextual judgment that current systems can’t reliably replicate.

Common barriers organizations encounter:

- Legacy technology: Older ERP systems often lack the APIs needed for clean integration, forcing workarounds that add fragility

- Fragmented data: Automation depends on consistent, structured data; organizations with siloed systems or inconsistent data formats see lower straight-through processing rates

- Non-standard documents: Vendor invoices that don’t follow standard formats challenge OCR accuracy and require manual review queues

- Regulatory complexity: Tax rules, multi-jurisdiction compliance, and audit trail requirements add layers that pure automation struggles to navigate

- Skills gaps: Finance teams often lack the technical fluency to configure, maintain, or troubleshoot automation tools without IT support

“The last mile of fund accounting automation — handling exceptions, regulatory edge cases, and judgment-dependent decisions — remains stubbornly resistant to full automation. The organizations that succeed treat this not as a failure of technology but as a design constraint that shapes how they build their human-AI workflows.” — Fund accounting automation research

Pro Tip: Build your automation program around a hybrid model from the start. Assign clear ownership for exception handling — a human-in-the-loop review queue that catches what the automated layer flags. This isn’t a workaround; it’s a design principle that makes the system more resilient and auditable.

The compliance automation guide covers how organizations structure these hybrid workflows for regulated environments. The key insight is that automation doesn’t replace judgment — it frees up the humans who exercise judgment by handling everything that doesn’t require it. Reviewing automation strategies and a broader business automation guide helps teams design systems that scale without accumulating technical debt.

Strategic implementation: Getting started and scaling automation

Having outlined the challenges, here’s how savvy organizations build automation roadmaps for sustained success.

The organizations that see the strongest ROI don’t try to automate everything at once. They start pilots with AP for quick payback, measure KPIs rigorously, and expand only after the first phase demonstrates stable performance. This sequenced approach reduces risk and builds organizational confidence in the technology.

A practical framework for launching and scaling finance automation:

- Select the right process first. Prioritize high-volume, rule-based workflows with clear inputs and outputs. AP invoice processing is the standard starting point for good reason — it’s measurable, repetitive, and the ROI is fast.

- Run a contained pilot. Limit scope to one process or one business unit. Define success metrics before you start, not after. Set a 90-day evaluation window.

- Measure KPIs against baseline. Track cost per transaction, processing time, error rate, and exception rate. Compare against pre-automation data collected before the pilot launched.

- Assign human oversight roles. Identify who handles exceptions, who monitors system performance, and who owns escalation. Automation without oversight creates blind spots.

- Expand to adjacent processes. Once AP is stable, extend to AR, then reconciliation, then reporting. Each phase builds on the data infrastructure and organizational learning from the last.

- Integrate with ERP and reporting systems. Automation that doesn’t feed clean data into your core financial systems creates reporting gaps. Integration is not optional at scale.

Pro Tip: Resist the temptation to automate complex, exception-heavy processes first. The quick wins from high-volume, rule-based tasks build the internal credibility and technical foundation needed to tackle harder problems later. Reviewing enterprise automation processes gives teams a clearer picture of where complexity tends to accumulate.

The ability to automate financial transactions at scale depends on having clean data, integrated systems, and a team that understands both the technology and the business rules it’s meant to enforce. Culture matters as much as tooling — teams that view automation as a threat rather than a support layer will find ways to work around it.

Rethinking automation: What most experts miss

Before moving to solutions, it’s worth looking past the headlines to what actually delivers results — and what doesn’t.

The automation conversation in finance has a tendency to swing between two extremes: either technology will replace the finance function entirely, or it’s too risky to trust with anything important. Both positions miss the practical reality. Research shows 42% of finance tasks are fully automatable, while 54% support only partial automation — meaning full autonomy is structurally impossible given the judgment requirements baked into financial decision-making.

What experienced practitioners know is that the real value of automation isn’t headcount reduction. It’s data quality and speed of insight. When reconciliation closes in one day instead of seven, finance leaders have six extra days to analyze what the numbers mean. That’s a strategic shift, not just an operational one.

The organizations that get the most from automation are those that redesign workflows around the technology rather than simply layering automation on top of existing processes. Exploring scalable automation solutions with this mindset changes what’s possible. The hybrid model — automated execution, human judgment — isn’t a compromise. It’s the architecture that actually works.

Connect with advanced automation solutions

If you’re ready to translate these strategies into action, Bitecode can help accelerate your automation journey with purpose-built tools for finance teams.

Bitecode’s enterprise automation solutions are designed for medium to large organizations that need scalable, configurable systems without multi-year development timelines. With up to 60% of the baseline system pre-built through modular components, finance teams can deploy faster and customize where it matters. The platform’s AI assistant for finance integrates directly into financial workflows, supporting exception handling, anomaly detection, and reporting automation. Whether your team is launching a first AP pilot or scaling across the enterprise, Bitecode provides the technical foundation to build without starting from zero.

Frequently asked questions

What processes are best suited for financial automation?

High-volume, rule-based processes like accounts payable, accounts receivable, reconciliations, and reporting deliver the fastest ROI because they have clear inputs, predictable outputs, and minimal judgment requirements. Prioritizing AP and AR for initial pilots also provides the fastest payback period, typically 4 to 7 months.

How quickly can organizations see ROI from finance automation?

Typical payback runs 4 to 7 months for AP automation pilots, with 111-287% ROI over three years documented across enterprise deployments in independent Forrester research. Results vary based on process volume, integration quality, and how rigorously KPIs are tracked from launch.

What are the main barriers to full financial automation?

Regulatory complexity, fragmented data, non-standard documents requiring human interpretation, and legacy ERP systems without modern APIs are the most common obstacles. Data fragmentation and regulatory hurdles consistently appear as the top barriers in enterprise automation assessments.

Is full AI autonomy possible in finance?

No — the judgment requirements embedded in financial decision-making make full autonomy structurally unrealistic. 54% of finance tasks support only partial automation, confirming that hybrid human-AI models are the practical standard, not a fallback position.