TL;DR:

- SaaS enables significant cost reductions and faster product launches in banking.

- Key features include automation, compliance modules, real-time analytics, and scalable architecture.

- Successful adoption requires workflow redesign, cross-functional teams, and organizational change management.

SaaS is not a generic cloud storage upgrade. For banks and financial institutions, it represents a structural shift in how operations run, how products reach market, and how compliance gets managed at scale. The misconception that SaaS simply moves existing software to the cloud undersells its actual impact. Banks that adopt purpose-built SaaS platforms are achieving 160% ROI alongside dramatic reductions in cost-to-serve and product launch timelines. This article breaks down how SaaS transforms financial operations, which features matter most, how it compares to Banking-as-a-Service (BaaS), and what blockchain integration actually requires in practice.

Key Takeaways

| Point | Details |

|---|---|

| SaaS slashes costs | Financial institutions see up to 50% lower serving costs thanks to SaaS solutions. |

| Faster product launches | SaaS enables banks to launch products up to ten times faster than legacy systems. |

| Blockchain integration needs middleware | Middleware and privacy engines are essential for secure and compliant blockchain adoption in banking. |

| Choose SaaS vs. BaaS wisely | Consider SaaS for internal efficiency and BaaS for customer-facing embedded finance. |

| Modular SaaS maximizes agility | Modular SaaS platforms make scaling and regulatory compliance easier for institutions. |

How SaaS transforms financial operations

The efficiency case for SaaS in banking is no longer theoretical. Institutions that have moved core operations to SaaS platforms are reporting measurable, repeatable gains across cost, speed, and return on investment. These are not edge cases. They reflect a structural shift in how financial services technology delivers value.

The numbers are direct. Banks adopting SaaS see 30-50% cost-to-serve reduction and product launch speeds that are 5-10x faster than legacy environments. Run costs drop by roughly 25%, and ROI reaches 160% over a measured period. These benchmarks come from institutions that replaced fragmented on-premise stacks with integrated, cloud-native platforms.

| Metric | Legacy systems | SaaS platforms |

|---|---|---|

| Cost-to-serve reduction | Baseline | 30-50% lower |

| Product launch speed | Baseline | 5-10x faster |

| Run cost change | Baseline | 25% lower |

| ROI | Variable | Up to 160% |

The operational benefits extend beyond raw cost savings. Understanding SaaS ROI and gains reveals that the compounding effect of faster iteration, reduced manual overhead, and automated compliance checks is what drives long-term value.

Practical benefits that institutions report include:

- Automated reconciliation reducing manual processing hours by significant margins

- Real-time transaction monitoring replacing batch-based oversight

- Centralized audit trails that simplify regulatory reporting

- Faster onboarding workflows for both customers and internal teams

For teams evaluating workflow optimization in fintech, the shift from reactive to proactive operations is the real transformation. SaaS relocates complexity into the vendor relationship rather than internal infrastructure, freeing engineering teams to focus on business-domain problems. When you factor in finance automation savings, the financial case for modernization becomes difficult to argue against.

Key SaaS features for banks and financial institutions

With clear evidence of efficiency gains, what SaaS features specifically drive these results? Not all SaaS platforms deliver equally. The institutions that see the strongest outcomes are those that prioritize specific capabilities from the start, rather than layering features onto a generic platform after deployment.

The core features that matter most in financial SaaS include:

- Process automation: Automating repetitive tasks like loan origination, KYC (Know Your Customer) checks, and payment reconciliation reduces both error rates and cycle times

- Regulatory compliance modules: Built-in compliance engines that update with regulatory changes reduce the burden on internal legal and risk teams

- Real-time analytics: Live dashboards and transaction monitoring give risk officers and executives actionable data without waiting for end-of-day reports

- Workflow integration: APIs that connect SaaS tools with core banking systems prevent data silos and enable straight-through processing

- Scalability: Cloud-native architecture means institutions can scale transaction volumes during peak periods without infrastructure investment

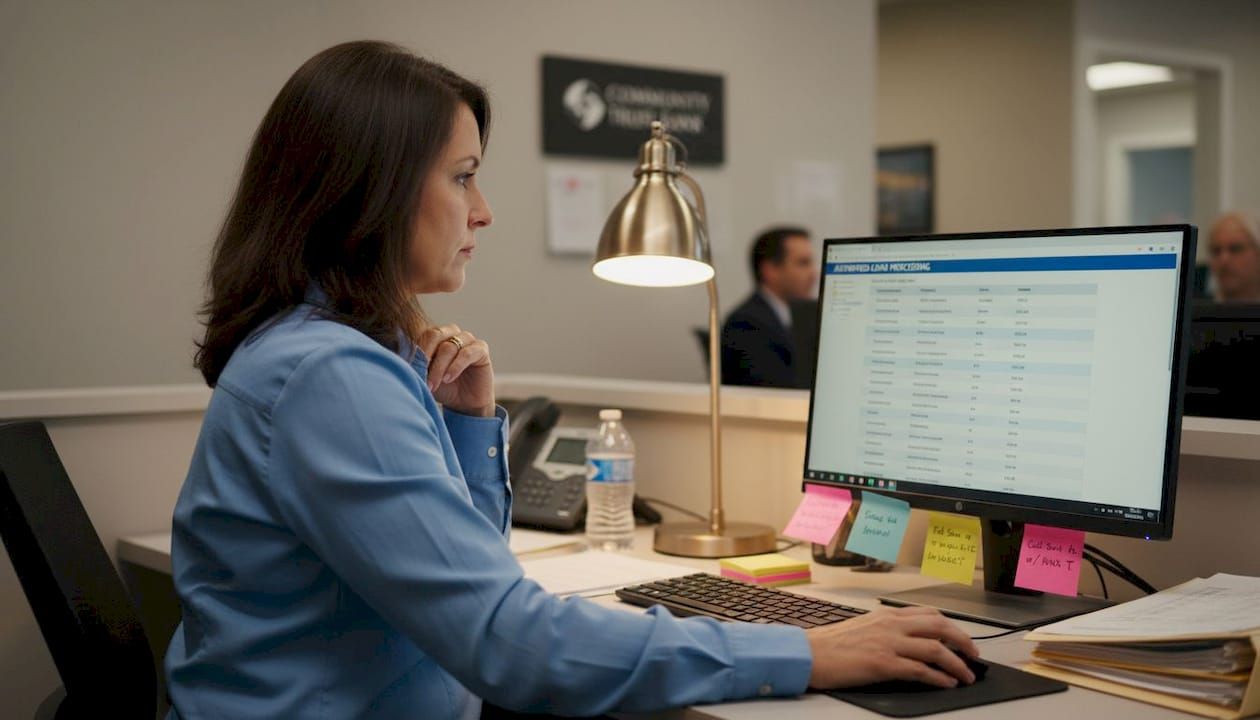

The impact of automation on loan processing is a useful benchmark. Community banks that adopted automating financial transactions practices have seen 27% faster loan processing and 42% lower operational costs. Those are not marginal improvements. They represent a fundamental change in how credit decisions get made and delivered.

For institutions evaluating scalable process automation, the architecture of the platform matters as much as the feature list. A modular SaaS foundation allows teams to activate capabilities incrementally, avoiding the big-bang deployment risk that has derailed many legacy modernization programs.

Pro Tip: When evaluating SaaS vendors, prioritize platforms with modular architecture. This lets your teams enable compliance, automation, and analytics features independently, reducing deployment risk and making it easier to adapt as regulations change. Reviewing best practices for enterprise software before vendor selection can prevent costly architectural mistakes.

Comparing SaaS and BaaS: Choosing the right model

Now that we have explored core SaaS features, it is crucial to understand how SaaS compares to other models like BaaS. Banking-as-a-Service is not a synonym for SaaS. The two models serve different strategic purposes, and choosing between them, or combining them, requires clarity on what the institution is actually trying to achieve.

SaaS offers predictable costs and focuses on internal operational efficiency. BaaS, by contrast, delivers full banking capabilities via APIs, enabling non-bank companies to offer financial products to their customers. SaaS optimizes what happens inside the institution. BaaS extends banking infrastructure outward.

| Dimension | SaaS | BaaS |

|---|---|---|

| Primary use | Internal operations | Customer-facing products |

| Cost model | Predictable subscription | Variable, API-based |

| Control | Moderate | Lower (shared with provider) |

| Compliance responsibility | Shared | Heavily shared with BaaS provider |

| Best for | Efficiency, automation | Embedded finance, fintech partnerships |

To evaluate which model fits your institution, work through these steps:

- Define whether the goal is internal efficiency or external product expansion

- Assess current compliance infrastructure and capacity to manage shared responsibility

- Evaluate API readiness and integration complexity with existing core systems

- Map revenue impact of each model against implementation timeline

- Pilot one capability area before committing to full platform migration

For institutions exploring embedded finance via APIs, BaaS opens significant revenue opportunities. But it also relocates compliance complexity into the vendor relationship in ways that require careful governance. Teams building secure financial software need to account for this before committing to a BaaS-first architecture.

Pro Tip: A modular approach lets institutions blend SaaS and BaaS benefits. Start with SaaS for internal automation, then layer BaaS capabilities for customer-facing features once the operational foundation is stable.

Blockchain integration: Real challenges and practical solutions

With SaaS and BaaS defined, blockchain integration is becoming a priority for banks. But the gap between blockchain’s promise and its practical implementation in regulated financial environments is wider than most technology roadmaps acknowledge.

The core integration challenges are structural, not just technical:

- Data structure mismatches: ISO 20022 messaging standards used in traditional banking do not map cleanly to distributed ledger formats, requiring translation layers

- Transaction irreversibility: Blockchain’s immutable ledger conflicts with banking’s need for chargebacks, reversals, and dispute resolution

- KYC/AML compliance gaps: Decentralized systems lack native identity verification, creating friction with Know Your Customer and Anti-Money Laundering (AML) obligations

- Chain fragmentation: Multiple competing blockchain networks create interoperability problems when institutions need cross-chain settlement

- Regulatory uncertainty: Evolving rules around digital assets and the Travel Rule add compliance overhead that changes faster than most integration timelines

“Hybrid middleware and compliance engines are more practical than direct chain integration for financial institutions. Addressing nuances like the Travel Rule and sanctions screening requires purpose-built layers between legacy systems and the blockchain network, not a direct connection.” — Blockchain integration analysis

Practical approaches involve building middleware that translates between banking protocols and ledger formats, implementing zero-knowledge (ZK) privacy layers to protect transaction data while maintaining auditability, and using processing system challenges frameworks to map integration points before writing a single line of code. Teams investing in blockchain application development consistently report that the compliance layer is more complex and more expensive than the blockchain layer itself.

What most institutions miss about SaaS adoption

After seeing the full landscape, here is what experienced teams know that most newcomers overlook: the technology is rarely the hard part. The hard part is workflow redesign, compliance alignment, and cross-functional coordination.

Institutions that stall on SaaS adoption typically share a common pattern. They evaluate platforms based on feature lists rather than integration depth. They prioritize short-term licensing savings over long-term architectural agility. And they underestimate the organizational change required to get value from automation. A platform that automates loan processing is only useful if the underwriting workflow has been redesigned to match.

For blockchain specifically, hybrid middleware and compliance engines are more practical than direct chain integration. Institutions that try to connect core banking systems directly to a blockchain network without an intermediate compliance layer consistently run into Travel Rule violations, sanctions screening gaps, and audit failures.

The institutions that move fastest are those that build cross-functional deployment teams from the start, combining technology, compliance, and operations ownership in a single working group. Reviewing SaaS adoption best practices before deployment, not after, is what separates institutions that accelerate work without accelerating chaos from those that stall mid-implementation.

Explore SaaS innovation with Bitecode

The efficiency gains, integration patterns, and architectural decisions covered in this article are exactly the territory Bitecode is built to navigate with financial institutions.

Bitecode’s modular platform starts with up to 60% of the baseline system pre-built, which means your teams spend less time on boilerplate and more time on business-domain complexity. Whether you need custom CRM solutions for client relationship management, AI workflow automation to streamline transaction processing, or a purpose-built blockchain payment system with compliance layers already integrated, Bitecode provides modular components that scale with your institution’s needs. The result is faster deployment, lower risk, and a foundation built for the operational demands of regulated financial services.

Frequently asked questions

What is SaaS for financial institutions?

SaaS for financial institutions delivers cloud-based software to streamline operations, automate transactions, and manage compliance while reducing costs. Banks using purpose-built SaaS platforms report up to 160% ROI alongside significant reductions in cost-to-serve.

How does SaaS differ from BaaS in banking?

SaaS optimizes internal operations with predictable subscription costs, while BaaS delivers full banking capabilities via APIs, enabling customer-facing financial products and embedded finance partnerships.

What are the biggest challenges with blockchain integration in SaaS?

Key challenges include data structure mismatches, transaction irreversibility conflicts, KYC/AML compliance gaps, and chain fragmentation. Middleware and zero-knowledge privacy layers are the most practical solutions.

Which SaaS features deliver the most value for banks?

Process automation, real-time analytics, regulatory compliance modules, and workflow integration deliver the strongest results. Community banks report 27% faster loan processing and 42% lower operational costs after implementing these capabilities.