TL;DR:

- Blockchain technology significantly reduces transaction settlement times and reconciliation costs.

- Permissioned and hybrid blockchains are preferred for regulated financial workflows due to better governance.

- Successful implementation requires starting with quantifiable friction points, legal clarity, and early compliance integration.

Walmart’s food traceability team once needed seven days to trace a mango through its supply chain. After deploying a blockchain-based ledger, that same trace took 2.2 seconds, delivering a 266% ROI over three years. That result has nothing to do with cryptocurrency. It reflects a broader shift now reaching banking, settlements, cross-border payments, and enterprise financial operations. Financial executives who still associate blockchain primarily with speculative tokens are working with an outdated model. This guide examines how distributed ledger technology is generating measurable returns in institutional finance, where the real friction points are, and how organizations can structure integrations that actually hold up under regulatory scrutiny.

![]()

Key Takeaways

| Point | Details |

|---|---|

| Blockchain reduces friction | DLT-based systems lower operational costs, minimize manual reconciliation, and speed up transactions. |

| Smart contracts drive automation | Automated settlements and payments reduce errors and enable real-time execution of financial agreements. |

| Governance and compliance are crucial | Permissioned and hybrid blockchains align best with regulatory frameworks and reduce integration risk. |

| ROI proven in pilots | Case studies with global banks and enterprises show measurable gains in efficiency, trust, and profitability. |

How blockchain is transforming financial processes

Blockchain technology, at its core, is a distributed ledger: a shared, append-only record of transactions maintained across multiple nodes without a single controlling authority. For financial operations, this architecture solves a problem that has persisted for decades. Traditional financial infrastructure relies on intermediary institutions (custodians, clearinghouses, correspondent banks) to verify and reconcile transactions. Each intermediary adds latency, cost, and the possibility of errors that require manual correction.

The European Central Bank has noted that blockchain enables decentralized, immutable ledgers for secure financial transactions, reducing the role of intermediaries through smart contracts that automate processes like payments and settlements. A smart contract is a self-executing program stored on the blockchain that carries out predefined actions when agreed conditions are met, with no human intervention required after deployment.

Two broad categories of blockchain matter for enterprise finance:

- Permissionless blockchains (like public Ethereum) are open to any participant. They offer maximum transparency but create governance and regulatory challenges that most financial institutions cannot accept.

- Permissioned blockchains (like Hyperledger Fabric or JPMorgan’s Quorum) restrict participation to vetted parties. They preserve control, enable regulatory auditability, and are far more practical for institutional deployment.

The security and audit advantages are concrete. Every transaction on a blockchain carries a cryptographic timestamp and a reference to the prior transaction block, creating an audit trail that cannot be altered without breaking the chain. For compliance teams, this replaces the labor-intensive process of cross-referencing multiple ledgers and calling counterparties for confirmation.

“The immutability of the ledger is not just a technical property. It is a governance mechanism. It relocates the burden of proof from manual reconciliation to cryptographic verification.”

The performance evidence is compelling. JPMorgan’s Quorum platform delivered an 85% client trust increase, and a documented cross-border payments pilot cut settlement times by 90% while reducing nostro account requirements by 62%. Understanding smart contract automation is essential before designing any of these workflows, because the contract logic determines how reliably the process executes under real-world conditions.

For teams focused on operational efficiency, the case is not theoretical. Blockchain efficiency in SaaS environments and enterprise systems shows consistent patterns: reduced reconciliation cycles, fewer exception handling events, and lower per-transaction costs at scale. The underlying mechanism is straightforward. Fewer intermediaries means fewer handoffs, and fewer handoffs means fewer failure points. Boosting financial transaction efficiency through blockchain integration is not about replacing every existing system at once. It is about identifying where the ledger’s properties solve a specific, measurable workflow problem.

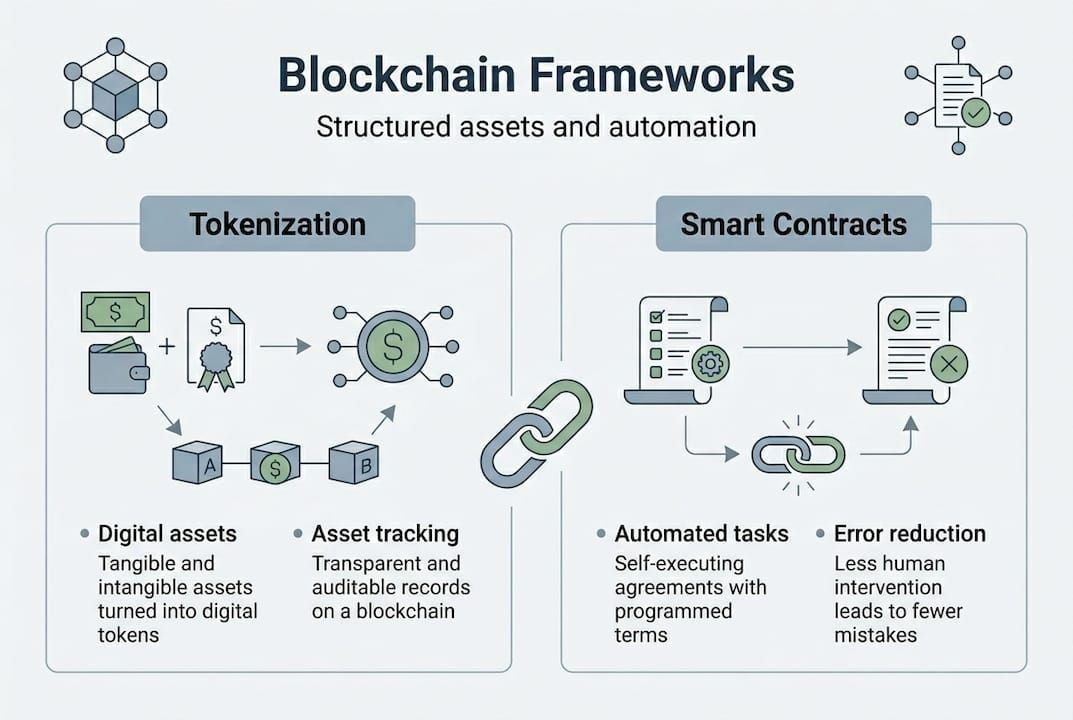

Tokenization and smart contract automation: Practical frameworks

Understanding blockchain’s architecture sets the foundation. Now it is worth examining tokenization and smart contracts in granular detail, because these are the two mechanisms that translate blockchain’s theoretical advantages into operational outcomes.

Tokenization is the process of representing a real-world asset (a bond, a receivable, a share, a piece of real estate) as a digital token on a distributed ledger. The token carries rights and attributes associated with the underlying asset, and those rights are enforced by the ledger’s rules rather than by a paper contract held in a vault somewhere. The ECB has documented that key methodologies include tokenization for full lifecycle management of assets including issuance, trading, and settlement on DLT, covering both permissioned and public blockchains, and hybrid models that balance transparency with control.

Full lifecycle management means the entire journey of an asset from creation to transfer to settlement can occur on the same ledger. This eliminates the need to synchronize data across multiple siloed systems, which is currently one of the largest sources of reconciliation cost in capital markets.

A structured deployment sequence for smart contract automation typically follows this order:

- Define the trigger conditions for each automated action, mapping them precisely to existing contractual terms.

- Select the appropriate blockchain environment, permissioned for regulated assets, hybrid for cross-institutional workflows.

- Deploy the contracts in a sandbox environment and test against edge cases including failed conditions, disputed inputs, and network interruptions.

- Integrate with existing financial systems using API layers that allow the blockchain layer to communicate with ERP platforms, payment rails, and compliance engines.

- Run a controlled pilot on a defined subset of transactions before scaling to full production volume.

Examining blockchain automation examples from enterprise deployments shows a consistent pattern: organizations that follow a sequential, phase-gated deployment approach achieve substantially better outcomes than those attempting broad simultaneous rollouts. Scalable financial automation requires this kind of disciplined sequencing to avoid compounding complexity.

The following table summarizes outcomes from documented blockchain pilot projects across financial use cases:

| Use case | Processing time reduction | Error rate reduction | Estimated ROI |

|---|---|---|---|

| Cross-border payment settlement | 90% | 40-55% | High |

| Trade finance reconciliation | 70% | 60% | Medium-high |

| Supply chain finance tracing | 99.9% (7 days to 2.2s) | 80%+ | 266% over 3 years |

| Equity settlement (tokenized) | 50-65% | 35% | Medium |

| KYC/AML data sharing | 40% | 45% | Medium |

Pro Tip: Consider hybrid blockchain models when deploying across multiple institutions or jurisdictions. A hybrid approach lets you keep sensitive transaction data on a permissioned layer while publishing settlement proofs to a public chain for independent auditability. This balances regulatory control with the transparency counterparties often require.

Challenges: Fragmentation, reconciliation, and regulatory hurdles

With practical frameworks defined, you also need to navigate emerging complexities around governance, legal standing, and technical integration. These are not edge cases. They surface regularly in production environments.

The fragmentation problem is most acute in permissionless networks. Multiple public blockchains operate in parallel without native interoperability, meaning an asset tokenized on one chain cannot easily interact with a contract deployed on another. Permissioned environments reduce this risk by design, but they introduce their own interoperability challenges when different institutions deploy incompatible DLT platforms.

The Banca d’Italia has raised a sharper concern: tokenization creates a reconciliation paradox where legal rights can diverge from token ownership, courts can override blockchain states, and smart contracts remain limited to narrow operational settings and are not legal substitutes for formal contracts. This is not a reason to avoid tokenization. It is a reason to design legal wrappers and governance structures before deploying on-chain logic.

“A token may represent a right, but a court adjudicates it. Organizations that treat the ledger as the final word on ownership are relocating legal complexity, not eliminating it.”

Common integration challenges that surface across deployments include:

- Data standardization failures, where off-chain data fed into smart contracts does not meet format or validation requirements.

- Governance gaps, where no clear authority exists to authorize contract updates when business rules change.

- Oracle dependency risk, where smart contracts relying on external data feeds inherit the reliability issues of those feeds.

- Regulatory misalignment, particularly where AML monitoring and data privacy requirements conflict with blockchain’s transparency properties.

- Change management friction, where operational teams resist adopting new reconciliation workflows built around on-chain verification.

Understanding financial compliance challenges in this context is critical, because compliance is not a layer added at the end of integration. It must be embedded from the architecture phase.

The comparison below maps the key risk dimensions across blockchain types:

| Dimension | Public (permissionless) | Permissioned | Hybrid |

|---|---|---|---|

| Legal risk | High (limited recourse) | Low (governed participants) | Medium |

| Regulatory compliance | Difficult | Manageable | Manageable |

| Operational complexity | High | Medium | Medium-high |

| Scalability | Variable | High | High |

| Interoperability | Fragmented | Platform-dependent | Structured |

For IT managers evaluating financial processing system risks, this comparison highlights why permissioned and hybrid architectures dominate serious enterprise deployments. The public chain is not irrelevant, but it is rarely the right starting point for regulated financial workflows.

Maximizing value: Integration strategies and measurable ROI

Once risks and complexity are understood, the next question is how organizations actually extract value through disciplined integration, not in theory but in production.

The empirical evidence is precise. Australian banks showed blockchain adoption positively impacts return on assets at a coefficient of 0.0025 (p=0.039) and return on equity at a coefficient of 0.0327 (p=0.002). These are statistically significant results, not anecdotal claims. For executive teams seeking board-level justification, these numbers translate directly to shareholder value arguments.

A structured integration approach for scaling blockchain from pilot to production typically follows these steps:

- Identify the highest-friction financial process in the current workflow, specifically one where reconciliation costs, settlement delays, or error rates are measurable and documented.

- Select a permissioned or hybrid DLT platform aligned with existing technology infrastructure and counterparty capabilities.

- Establish interoperability standards at the outset, ensuring the blockchain layer can communicate with existing ERP, payment, and compliance systems without bespoke integrations for each connection.

- Deploy a time-bound pilot with defined success metrics: error rate, settlement time, reconciliation cost per transaction, and audit compliance rate.

- Conduct a regulatory alignment review with legal counsel familiar with MiCAR (Markets in Crypto-Assets Regulation) and relevant AML frameworks before scaling.

- Scale incrementally, expanding to adjacent process areas rather than attempting enterprise-wide deployment before the pilot model is fully validated.

Prioritizing permissioned DLT for control, ensuring interoperability standards, maintaining robust governance for risks, aligning with MiCAR, and focusing on high-volume processes like payments and settlement are the integration priorities consistently identified in rigorous research.

Understanding finance automation ROI requires separating short-term cost reduction from long-term structural advantage. The cross-border settlement case cutting processing time by 90% and nostro accounts by 62% is a structural change, not a one-time saving. Reviewing workflow optimization guides helps teams map those structural benefits to specific process areas before committing budget to a platform.

Pro Tip: Focus blockchain integration on processes where transaction volume is high, intermediary costs are significant, and reconciliation errors create measurable downstream costs. Applying distributed ledger technology to low-volume, low-friction processes rarely justifies the integration overhead. Use an automation checklist to qualify candidate processes before committing to architecture decisions.

A fresh perspective: Why most blockchain pilots fail—and what actually works

The uncomfortable reality is that most blockchain pilots in financial institutions fail not because the technology underperforms, but because the problem definition was wrong from the start. Teams select blockchain because it signals innovation, not because it is the right tool for the specific friction they face.

The tokenization illusion is a specific version of this problem. Tokenization risks adding reconciliation layers rather than removing them when the legal and operational infrastructure surrounding the token is not designed with the same rigor as the on-chain logic. You end up with two systems of record that periodically disagree, which is precisely the problem blockchain was supposed to solve.

Successful deployments share a common pattern: they start with a workflow where the friction is transactional and quantifiable, they build legal clarity before writing contract code, and they treat user experience as a first-class engineering requirement rather than a cosmetic concern. Regulatory alignment, as addressed in depth through blockchain compliance frameworks, must be woven into the architecture from day one rather than retrofitted after deployment.

The organizations generating real returns are not blockchaining everything. They are applying distributed ledger technology selectively, at exactly the points where intermediary costs and reconciliation failures are largest, and they are building governance structures that can survive legal scrutiny. Start small, measure rigorously, and integrate compliance early. That is what works.

Take the next step: Secure, scalable blockchain finance solutions

The integration path from pilot to production is complex, but it does not have to mean starting from zero. Bitecode’s modular platform allows financial organizations to deploy blockchain payment solutions with up to 60% of the baseline system already structured, shortening development cycles without sacrificing the customization that regulated environments demand.

For teams that need to align blockchain infrastructure with client relationship workflows, Bitecode’s custom CRM solutions integrate directly with financial processing modules, giving operations and compliance teams a unified view of transaction data. The platform’s AI assistant module adds an intelligent automation layer that can surface reconciliation exceptions, flag compliance risks in real time, and reduce the manual workload that traditional financial systems demand. If your organization is ready to move from pilot thinking to production-grade deployment, Bitecode provides the modular foundation to do it securely and at scale.

Frequently asked questions

What are the biggest benefits of blockchain in finance?

Blockchain reduces intermediary costs and enables faster settlements through smart contract automation, while the immutable ledger provides auditable transaction records that lower compliance overhead across financial operations.

Is blockchain compliant with existing financial regulations?

Compliance depends heavily on architecture choices. Permissioned and hybrid DLT models are designed to align with regulatory frameworks like MiCAR, giving institutions governance control and auditability that public chains cannot reliably provide.

What risks should financial executives anticipate with blockchain projects?

Expect network fragmentation and reconciliation paradoxes where legal rights diverge from token states, combined with smart contract limitations that prevent on-chain logic from serving as a full substitute for formal legal contracts.

How can organizations measure ROI from blockchain implementation?

Track changes in settlement time, reconciliation cost per transaction, and error rates after each pilot phase. Australian banks documented statistically significant improvements in both ROA and ROE, providing a benchmark framework for connecting blockchain adoption to core financial performance indicators.