TL;DR:

- Most organizations have scaled RegTech across their operations but often misunderstand its proactive, data-driven nature. Agentic AI and layered technologies enhance compliance efficiency, accuracy, and strategic risk management, transforming regulation into business intelligence. External regulation increases pressure for structured, machine-readable data, requiring firms to prioritize data architecture and regulatory change management when implementing RegTech solutions.

Ninety-five percent of financial institutions have already scaled RegTech enterprise-wide, yet a surprising number of business leaders and compliance officers still struggle to articulate what regulatory technology actually is, let alone how it differs from the compliance software they already use. That confusion is costly. Organizations that misidentify RegTech as just another digitization tool miss the deeper operational shift it enables: moving compliance from reactive paperwork management to proactive, data-driven risk intelligence. This article cuts through the noise, offering a clear definition, a look at the technologies driving 2026’s RegTech capabilities, and practical guidance for leaders ready to act.

Key takeaways

| Point | Details |

|---|---|

| RegTech is proactive, not reactive | It automates regulatory data flows, reporting, and risk monitoring rather than simply digitizing existing evidence. |

| Agentic AI changes the compliance game | Autonomous AI systems can now investigate compliance alerts end-to-end, reducing false positives by over 75%. |

| Financial crime leads adoption | Sanctions screening and AML monitoring carry the highest adoption score (68%), delivering early ROI. |

| Regulators are adopting RegTech too | The UK FCA’s AI and automated data feed initiatives mean firms need RegTech strategies that align with regulator expectations. |

| Implementation starts with data flows | Successful deployments map regulatory data from source systems through validation to audit-ready submissions. |

What is regulatory technology and what does it do

The definition of regulatory technology, or RegTech, is straightforward at its core: it is the application of technology to help organizations manage regulatory compliance more efficiently, accurately, and proactively. But that definition only becomes useful when you understand what it covers in practice.

Core RegTech categories include regulatory reporting automation, sanctions and AML controls, regulatory change management, and identity verification. Each category addresses a distinct compliance bottleneck. Regulatory reporting automation, for example, pulls data from source systems, applies the correct jurisdiction-specific rules, and submits compliant filings without manual intervention. AML transaction monitoring scans millions of records for suspicious patterns in real time, something no human team can replicate at scale.

What separates RegTech from generic compliance software is its orientation toward regulatory data flows rather than internal process management. Generic compliance tools help teams track policies, document procedures, and store evidence. RegTech, by contrast, is designed around the regulatory requirement itself. It asks: what data does the regulator need, in what format, by what deadline, and how do we get there with minimal human error?

- Regulatory reporting automation: Generates and submits structured reports to regulators, pulling from multiple source systems and applying jurisdiction-specific formatting rules.

- Sanctions and AML controls: Screens customers, transactions, and counterparties against sanctions lists and monitors transaction flows for suspicious behavior patterns.

- Regulatory change management: Ingests new regulations or rule updates, assesses their applicability to the business, and maps required changes to downstream policies and systems.

- Identity verification and KYC: Automates customer onboarding checks against identity documents, watchlists, and risk indicators.

Pro Tip: When evaluating a RegTech vendor, ask them to walk through a regulatory data flow end-to-end, from source system extraction through validation to submission. If they can not demonstrate that clearly, the product likely relocates complexity into the vendor relationship rather than solving it.

The technology powering modern RegTech in 2026

Modern RegTech is not a single technology. It is a layered architecture, and understanding those layers helps compliance officers evaluate vendor claims with more precision.

| Technology | Role in RegTech | Contrast with legacy compliance tools |

|---|---|---|

| Agentic AI | Autonomously investigates alerts, executes multi-step workflows, delivers completed cases with confidence scores | Legacy tools flag alerts for human review; humans do all investigation steps |

| Machine learning | Detects transaction anomalies, scores risk, reduces false positives dynamically | Rule-based systems generate fixed alerts regardless of evolving patterns |

| Vector databases | Enables semantic search across regulatory text for change management and policy mapping | Keyword search returns incomplete matches across large regulatory document sets |

| Blockchain | Creates immutable audit trails for transactions and regulatory submissions | Centralized logs are mutable and vulnerable to tampering |

| Natural language processing | Ingests and parses regulatory text automatically, extracting rules and applicability criteria | Manual review of regulatory publications by compliance teams |

The most significant development in 2026 is the emergence of Agentic AI in compliance workflows. Unlike traditional AI that surfaces an alert and waits for a human decision, Agentic AI executes the entire investigation autonomously. It pulls transaction records, cross-references counterparty data, applies regulatory criteria, and delivers a completed case file with a recommendation and confidence score, all in milliseconds. That is not incremental efficiency. It is a fundamental shift in how compliance work gets done.

This architecture also enables something traditional compliance technology cannot: predictive compliance. By continuously ingesting regulatory publications through NLP pipelines and mapping changes to internal systems automatically, RegTech platforms can alert teams to upcoming compliance gaps before the enforcement date arrives. The difference between reactive and proactive compliance is often measured in six-figure regulatory fines.

Pro Tip: When assessing vendors on AI capabilities, specifically ask whether their AI operates as an autonomous agent or as a decision-support tool. The distinction matters enormously for staffing models and audit trail requirements, since regulators increasingly expect documented evidence of how automated decisions were made.

For deeper context on how AI reshapes risk management, the architecture principles extend well beyond compliance into broader enterprise risk functions.

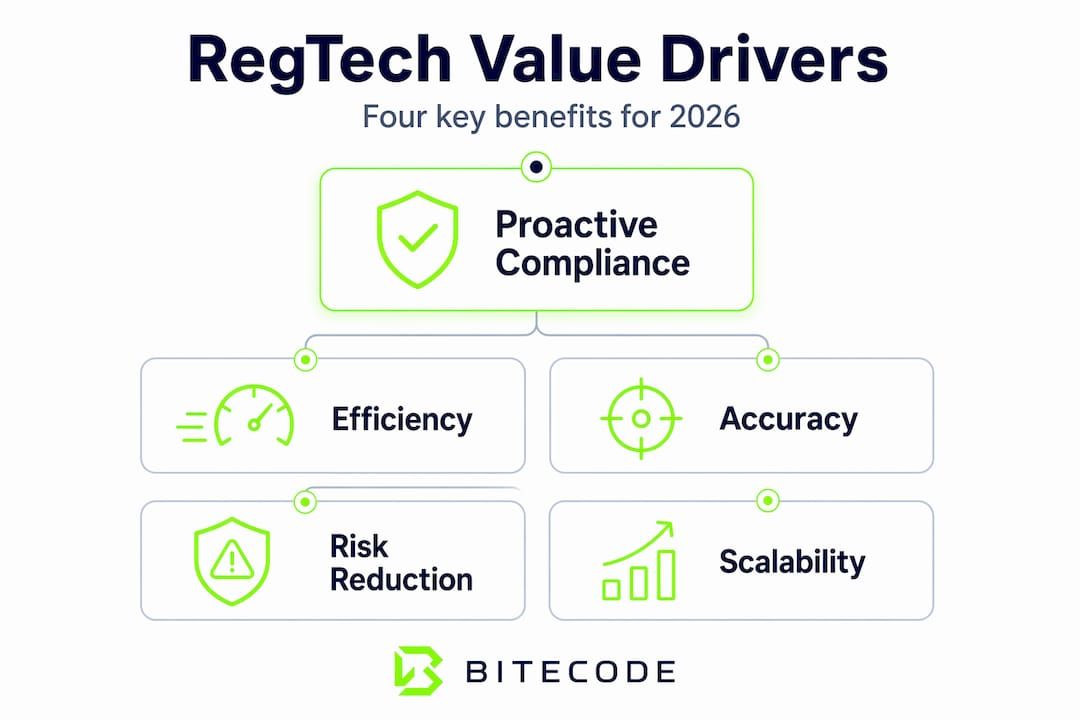

Key benefits and business impacts of RegTech

The business case for regulatory technology rests on four distinct value drivers. Understanding each separately prevents organizations from underestimating the total return on investment.

1. Efficiency and cost reduction. Automated workflows eliminate the manual effort of data aggregation, formatting, and submission across multiple jurisdictions. Teams that previously spent weeks preparing quarterly regulatory reports can redirect that capacity to higher-judgment work. The efficiency gains compound as the organization scales, since the technology handles increasing data volumes without proportional headcount increases.

2. Accuracy and audit readiness. Manual processes introduce errors at every handoff point. RegTech platforms improve reporting accuracy by applying consistent rules automatically and maintaining complete audit trails at every processing step. When a regulator requests evidence during an examination, the system can generate a full data lineage report immediately rather than requiring weeks of manual reconstruction.

3. Proactive risk monitoring. This is where RegTech’s financial crime capabilities demonstrate clear ROI. Financial crime controls carry the highest adoption score among RegTech domains at 68%, precisely because sanctions screening and AML monitoring deliver measurable risk reduction and early breach prevention. Organizations that detect suspicious patterns before transactions settle avoid not just fines but reputational damage.

4. Strategic intelligence. Perhaps the most underappreciated benefit: RegTech transforms compliance from a cost center into a source of business intelligence. The same data flows that power regulatory reporting also reveal operational patterns, customer risk concentrations, and process inefficiencies that are invisible to manual processes. Compliance data, properly surfaced, accelerates executive decision-making.

“RegTech is evolving compliance from a control function into a strategic intelligence-led business enabler.” — RegTech Global State Report 2026

These four drivers collectively reframe the RegTech investment decision. Organizations that evaluate RegTech purely on compliance cost savings are measuring the smallest part of the value pool.

The regulatory landscape driving RegTech adoption in 2026

The external environment is not just tolerating RegTech adoption. It is actively accelerating it. Regulatory complexity has increased substantially over the past decade, with data reporting requirements multiplying across financial services, healthcare, and digital asset markets simultaneously.

The adoption statistics make that pressure visible. 95% of financial institutions have now scaled RegTech usage across the enterprise, based on a 2026 survey of 300 senior compliance leaders and 100 RegTech vendors. That figure represents a technology that has crossed the maturity threshold from experimental to operational.

Regulators themselves are adopting the same technologies. The UK FCA’s 2026 initiatives include generative AI document review, a sandbox for automated data exchange between firms and the regulator, and broader plans to use AI to modernize supervision. This matters for compliance officers because it changes what data regulators will expect firms to provide, in what format, and at what frequency.

The SupTech versus RegTech distinction is increasingly relevant here. SupTech refers to the technologies regulators use to supervise firms, while RegTech refers to what firms use to manage their obligations. As regulators invest in SupTech, the data firms submit must meet higher standards for structure, completeness, and machine-readability. A RegTech strategy built around PDF report generation will increasingly fail to meet those standards.

| Dimension | RegTech (firm-facing) | SupTech (regulator-facing) |

|---|---|---|

| Primary user | Compliance teams at regulated firms | Regulatory supervisors and examiners |

| Core function | Automate data collection, reporting, and monitoring | Analyze firm-submitted data for supervisory risk signals |

| Data direction | Outbound to regulators | Inbound from regulated firms |

| 2026 trend | Agentic AI, real-time monitoring | AI document review, automated data feeds |

The implication for firms is clear. RegTech investments must be designed not just to satisfy today’s reporting templates but to produce structured, machine-readable data that will integrate with regulators’ own AI systems as those systems mature.

Implementing RegTech: guidance for business leaders

Most RegTech implementations that fail do so not because the technology is inadequate but because the deployment strategy treats RegTech as a software purchase rather than a data architecture project. The distinction matters.

Successful implementations start with regulatory data flows. That means mapping which source systems hold the data each regulatory requirement demands, understanding how that data must be transformed and validated before submission, and documenting the audit trail requirements at each step. Source mapping and validation are foundational, and vendors that skip this discovery phase produce integrations that break with every system upgrade.

Regulatory change management deserves particular attention. Many organizations buy change management tools that track regulatory publications without connecting those changes to downstream systems. That is only half the job. Effective change management requires linking each rule update to the specific policies, technology configurations, and reporting processes it affects, so that the operational impact of a new rule is visible before the compliance deadline.

- Prioritize data integration over front-end features. A RegTech platform with excellent dashboards but weak source system connectivity will always require manual data preparation, which defeats the primary efficiency purpose.

- Evaluate vendor knowledge of your specific regulatory regime. A vendor who understands MiFID II reporting or Basel IV capital calculations in detail will configure the system correctly. A vendor offering generic compliance software will require your team to encode every rule manually.

- Design for regulator interaction from the start. Consider what data your regulators are already requesting and what formats they accept. Aligning your RegTech architecture to those requirements now avoids costly retrofitting as SupTech mandates evolve.

- Build audit trail requirements into every workflow. The audit trail is not a reporting feature. It is an operational necessity that regulators will examine during supervisory reviews.

Pro Tip: Before selecting a RegTech vendor, run a structured proof of concept against one live regulatory data flow. Not a demo with sample data. A real workflow using your actual source systems and a current regulatory submission format. The gaps you discover will tell you more about vendor fit than any RFP response.

My take on where RegTech is really heading

I’ve watched organizations reduce RegTech to a cost-cutting argument, and it consistently leads to underinvestment. The real opportunity is not saving headcount on manual reporting. It’s creating a compliance function that generates the kind of intelligence executives actually use to make faster, better-informed decisions.

What I find genuinely exciting about Agentic AI in this space is how it challenges the assumption that compliance requires constant human judgment at every step. Most compliance decisions below the threshold of genuine novelty follow deterministic logic. Agentic AI handles that logic faster and more consistently than any team can. That frees compliance professionals to focus on interpretation, regulatory relationships, and edge cases where experience and judgment actually matter.

The honest challenge I see is data quality. Organizations that have spent years with fragmented source systems and inconsistent data definitions cannot drop a RegTech platform on top and expect clean results. The technology surfaces those issues rather than hiding them. That is useful, but it means the first phase of many implementations is actually a data remediation project. Leadership teams that understand this upfront avoid the frustration of blaming the technology for problems that pre-date it.

My pragmatic advice: start with the regulatory domain where your data is cleanest and your reporting obligations are most predictable. Build confidence there, establish the data architecture patterns that work for your organization, then expand. Trying to automate every compliance function simultaneously accelerates work without accelerating the foundations those workflows depend on.

— Bitecode

Build your RegTech foundation with Bitecode

Regulatory compliance at scale demands more than point solutions. It demands a connected system where financial processing, audit workflows, AI-driven monitoring, and blockchain-backed transaction trails operate from a shared data foundation.

Bitecode’s modular platform gives compliance-focused organizations a head start. The financial software modules cover accounting, audit, and subscription management with compliance-grade audit trails built in from day one. The AI assistant module enables automated regulatory workflow processing and alert investigation, while the blockchain payment module creates the immutable transaction records regulators increasingly expect. With up to 60% of the baseline system pre-built, organizations can move from scoping to deployment in weeks rather than quarters, without sacrificing the configurability that complex regulatory requirements demand.

FAQ

What is regulatory technology in simple terms?

Regulatory technology, or RegTech, is software that automates how organizations manage regulatory compliance, covering reporting, monitoring, change management, and identity verification. It uses technologies like AI, machine learning, and blockchain to reduce manual effort and improve accuracy.

How does RegTech differ from compliance software?

Standard compliance software digitizes internal processes and stores evidence. RegTech is oriented toward external regulatory requirements, automating the data flows, formatting, and submissions that regulators actually receive.

What are the main examples of regulatory technology?

The leading examples include AML transaction monitoring systems, sanctions screening tools, automated regulatory reporting platforms, KYC identity verification systems, and regulatory change management tools that map rule updates to operational systems.

What are the benefits of regulatory technology for firms?

The primary benefits are reduced manual effort in compliance reporting, improved accuracy and audit readiness, proactive financial crime detection, and the ability to treat compliance data as a source of business intelligence rather than a cost-only function.

How widely adopted is RegTech in financial services?

Adoption is near-universal in financial services, with 95% of institutions having scaled RegTech enterprise-wide as of 2026, according to a survey of 300 senior compliance leaders.