TL;DR:

- Fintech software consists of both customer-facing platforms and internal infrastructure that support regulated financial activities. Its effectiveness relies on a complex distributed architecture emphasizing robust back-end systems and seamless integration with core banking and third-party services. Organizations should evaluate vendor maturity, compliance, and AI capabilities while treating implementation as a business problem first, not just a technology challenge.

Fintech software is defined as technology that enables, supports, or replaces regulated financial products and services through digital applications and data processing. The White House defines fintech firms as non-bank companies using technology to deliver payments, lending, digital banking, investment management, and blockchain services under regulatory oversight. For business owners and executives, understanding what fintech software actually does, and how it works beneath the surface, is the prerequisite to making sound decisions about adoption, integration, and vendor selection. Platforms like Mambu, tools from Intuit, and infrastructure from IBM illustrate just how broad and operationally significant this category has become.

What is fintech software and what does it actually include?

Fintech software encompasses two distinct layers that executives must evaluate separately. The first is the customer-facing layer: digital wallets, mobile banking apps, lending platforms, and investment dashboards. The second is the internal infrastructure layer, which includes credit scoring engines, compliance monitoring systems, and fraud detection pipelines. Both layers are essential for regulated financial services to function correctly and legally.

Most executives focus on the interface. That is a mistake. The interface is the smallest part of the system. What determines operational risk, regulatory exposure, and long-term scalability is the back-end architecture. A digital wallet that processes payments in milliseconds is only possible because of distributed transaction systems, real-time ledger reconciliation, and audit logging running underneath it.

Fintech software also operates in contexts that are not consumer-facing at all. According to Intuit’s career and industry guidance, fintech software frequently runs embedded within business operations, powering payroll systems, expense management tools, and B2B payment rails that most end users never directly interact with. This embedded layer is where many organizations find the highest return on fintech investment.

- Customer-facing platforms: Digital wallets, mobile banking apps, peer-to-peer lending interfaces, robo-advisors, and buy-now-pay-later checkout flows

- Back-end infrastructure: Credit scoring models, anti-money laundering (AML) engines, KYC verification pipelines, fraud detection systems, and regulatory reporting modules

- Embedded fintech: Payroll processing, accounts payable automation, treasury management, and B2B payment orchestration built into enterprise workflows

Pro Tip: When evaluating any fintech software vendor, request a technical architecture overview that covers both the user interface and the back-end compliance and data processing systems. Vendors who cannot clearly explain the back-end layer are putting regulatory risk into your organization.

How does fintech software work technically?

Fintech applications run hundreds of interconnected systems with strict performance and security requirements, making what appears to be a simple balance check or payment confirmation the result of dozens of coordinated service calls. This distributed architecture is what makes fintech software fundamentally different from conventional enterprise software.

The core technical challenge is idempotency. Financial software handling payments and ledger activities must ensure idempotency and eventual consistency to prevent double processing during retries or network delays. In practice, this means every transaction must carry a unique identifier that allows the system to recognize and reject duplicate requests without failing the user experience. Getting this wrong produces duplicate charges, reconciliation failures, and regulatory violations.

Integration complexity is the second major technical dimension. Effective fintech software connects with core banking systems, third-party KYC providers, payment processors, CRM platforms, analytics engines, and notification services. Each integration point introduces a potential failure mode. This is why integration and load testing are ongoing operational priorities, not one-time pre-launch activities.

| System component | Function | Failure risk if absent |

|---|---|---|

| Transaction processor | Executes and records payments in real time | Duplicate charges, lost transactions |

| Idempotency layer | Prevents duplicate processing on retries | Double billing, ledger errors |

| KYC/AML engine | Verifies identity and monitors for suspicious activity | Regulatory penalties, fraud exposure |

| Compliance reporting module | Generates audit trails and regulatory filings | Legal liability, license revocation |

| Fraud detection pipeline | Flags anomalous transactions in real time | Financial losses, reputational damage |

Pro Tip: Before signing a fintech software contract, ask the vendor for their service level agreement (SLA) on transaction processing latency and uptime. Any SLA below 99.9% uptime for a payment-critical system is a risk that belongs in your due diligence report.

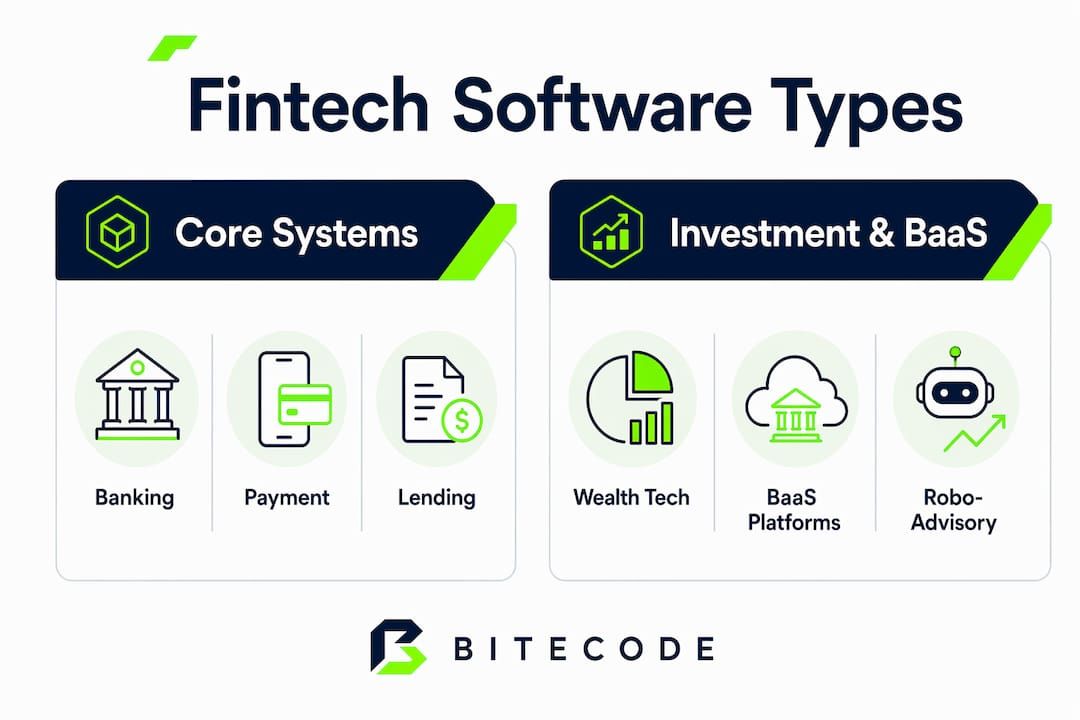

What types of fintech software solutions are available?

The fintech software market segments into four primary categories, each serving distinct operational needs. Understanding these categories prevents the common executive error of selecting a platform built for a different use case.

Core banking platforms replace or augment legacy banking infrastructure. Mambu’s composable SaaS platform supports deposits, lending, payments, and new product launches with lower overhead than traditional core systems. The composable model means financial institutions can configure and swap individual capabilities without rebuilding the entire system. This is the architectural shift that allows challenger banks to launch new products in weeks rather than quarters.

Payment processing software handles transaction routing, settlement, and reconciliation. This category includes payment gateways, payment orchestration layers, and cross-border payment rails. The distinction between a payment gateway and a payment orchestration platform matters operationally: gateways connect to a single processor, while orchestration platforms route transactions across multiple processors based on cost, geography, and success rate.

Lending platforms automate loan origination, underwriting, credit decisioning, and servicing. These platforms integrate with credit bureaus, income verification services, and document management systems. The degree of automation in the underwriting workflow directly determines how quickly a lender can scale without proportionally increasing headcount.

Investment management and wealth tech tools power portfolio management, robo-advisory services, and trading infrastructure. These systems require real-time market data feeds, risk modeling engines, and regulatory reporting capabilities specific to securities law.

| Software type | Primary use case | Deployment model | Key differentiator |

|---|---|---|---|

| Core banking platform | Deposits, lending, account management | SaaS / cloud-native | Composability and speed of product configuration |

| Payment processing | Transaction routing and settlement | API-first / embedded | Multi-processor orchestration and global reach |

| Lending platform | Loan origination and underwriting | SaaS / on-premise | Automation depth in credit decisioning |

| Investment management | Portfolio management and trading | SaaS / hybrid | Real-time data integration and compliance reporting |

| Banking-as-a-Service (BaaS) | Embedded finance for non-bank businesses | API / white-label | Speed of market entry for non-financial companies |

Banking-as-a-Service (BaaS) deserves specific attention. BaaS platforms allow non-financial businesses to embed financial products, such as branded debit cards, lending, or insurance, directly into their existing customer experience. Cloud and BaaS technologies have made this model accessible to mid-market companies that previously lacked the regulatory infrastructure to offer financial products.

How to evaluate and implement fintech software solutions

The build-versus-integrate decision is the first strategic choice any organization faces when adopting fintech software. The correct answer depends on regulatory exposure and the degree of business differentiation required. Standardized regulated components like KYC verification and payment gateways are almost always better integrated as mature vendor solutions. Building these from scratch relocates compliance risk into your engineering team, which is rarely where it belongs.

Custom development makes sense for the logic that differentiates your product: proprietary credit models, unique workflow automation, or domain-specific risk scoring. This is where in-house engineering investment produces durable competitive advantage. Everything else is boilerplate that a vendor can maintain more cost-effectively.

Practical evaluation criteria for fintech software selection:

- Regulatory readiness: Does the vendor hold relevant certifications (PCI DSS, SOC 2, ISO 27001)? Can they demonstrate compliance with the jurisdictions where you operate?

- Integration architecture: Does the platform expose well-documented APIs? What is the vendor’s track record on third-party integrations with your existing core systems?

- Vendor maturity: How long has the vendor operated in production environments at scale? Reference checks with existing enterprise clients are non-negotiable.

- Testing and monitoring: Does the vendor support integration testing environments, load testing, and real-time monitoring dashboards? Continuous testing of the entire product ecosystem is a requirement, not a feature.

- AI and automation capabilities: AI-powered solutions now support transaction monitoring, fraud prevention, and regulatory compliance at a level that manual processes cannot match. Evaluate whether the platform’s AI capabilities are native or bolted on.

Measuring implementation success requires tracking three dimensions: operational efficiency (processing time, error rates, manual touchpoints eliminated), risk metrics (fraud detection rates, compliance incident frequency), and customer experience indicators (transaction success rates, support ticket volume). Organizations that automate financial transactions report measurable gains across all three dimensions when the implementation is scoped correctly.

Key takeaways

Fintech software is defined by the financial activities it enables and the compliance obligations it carries, not by how its interface looks or how simple the user experience feels.

| Point | Details |

|---|---|

| Dual-layer architecture | Evaluate both customer-facing platforms and back-end compliance infrastructure before selecting any vendor. |

| Idempotency is non-negotiable | Payment systems must prevent duplicate processing; confirm this capability explicitly with any vendor. |

| Build vs. integrate | Integrate regulated components like KYC; build only the logic that creates genuine product differentiation. |

| Vendor maturity matters | Certifications, reference clients, and SLA terms are the three non-negotiable due diligence checkpoints. |

| AI enhances operations | Native AI capabilities for fraud detection and compliance monitoring are now a baseline expectation, not a premium feature. |

What Bitecode has learned from fintech software complexity

The most consistent mistake organizations make when adopting fintech software is underestimating integration complexity. The interface looks simple. The procurement conversation focuses on features. Then the implementation begins, and teams discover that connecting a new lending platform to a legacy core banking system requires months of custom middleware work that no one budgeted for.

Cloud-native, composable platforms like Mambu have genuinely changed what is possible in terms of speed and flexibility. But composability does not eliminate complexity. It relocates it. Instead of managing a monolithic system, teams manage a network of integrated services, each with its own SLA, API versioning cycle, and vendor relationship. That is a different kind of complexity, and in some ways a harder one to govern.

The organizations that implement fintech software most effectively treat it as a business-domain problem first and a technology problem second. They define the financial workflows they need to support, the regulatory obligations they must meet, and the customer experience they intend to deliver. Then they select technology that fits those constraints, rather than selecting technology and hoping the business requirements adapt.

AI and automation are accelerating the pace of change in this space. The step-by-step application of AI in fintech is no longer theoretical. Transaction monitoring, credit decisioning, and compliance reporting are all being augmented by machine learning models that improve with operational data. The executives who treat this as a long-term infrastructure investment, rather than a short-term cost reduction exercise, are the ones building durable competitive positions.

The practical advice is this: start with a modular foundation that covers your regulated baseline, then build differentiation on top of it. Do not attempt to greenfield a full fintech stack unless you have the engineering depth and regulatory expertise to sustain it. Most organizations do not, and the ones that discover this mid-project pay a significant price.

— Bitecode

How Bitecode accelerates fintech software development

Bitecode builds custom fintech software solutions using a modular foundation that starts projects with up to 60% of the baseline system pre-built. That means teams spend engineering time on business-domain complexity, not boilerplate infrastructure.

For organizations building financial workflows, Bitecode’s AI Assistant module provides a production-ready chat interface for workflow automation, transaction monitoring support, and compliance query handling. For companies requiring payment infrastructure, the blockchain payment system module delivers a pre-built, auditable payment layer that integrates with existing financial systems. Both modules are designed to accelerate fintech software development without accelerating chaos. Explore Bitecode’s fintech module catalog to identify where pre-built components can reduce your time to production.

FAQ

What is fintech software in simple terms?

Fintech software is technology that enables or supports regulated financial services, including payments, lending, banking, and investment management, through digital applications and data processing systems.

How does fintech software work behind the scenes?

Fintech software runs distributed systems that handle real-time transaction processing, identity verification, fraud detection, and compliance reporting simultaneously. What appears as a simple payment confirmation involves dozens of coordinated service calls across integrated platforms.

What are the main types of fintech software solutions?

The primary categories are core banking platforms, payment processing software, lending platforms, investment management tools, and Banking-as-a-Service (BaaS) platforms. Each serves distinct operational needs and carries different integration and compliance requirements.

What is the difference between building and integrating fintech software?

Regulated components like KYC verification and payment gateways are typically integrated from mature vendor solutions, while proprietary business logic such as custom credit models is built in-house. This division aligns regulatory risk with the parties best equipped to manage it.

Why does fintech software require specialized development expertise?

Fintech software must satisfy strict requirements for idempotency, auditability, latency, and regulatory compliance that standard enterprise software does not face. These constraints require engineering teams with direct experience in financial systems architecture and compliance frameworks.