TL;DR:

- Fintech digitalization involves a comprehensive transformation of how financial services are designed, delivered, and governed, extending beyond mobile apps to an ecosystem of technologies like AI, blockchain, and embedded finance.

- Organizations that adopt modular architectures, embed governance early, and embrace reverse integration gain significant competitive advantages while accelerating product innovation and reducing costs.

Fintech digitalization is not a synonym for mobile banking or a flashy payments app. It is a structural shift in how financial services are built, delivered, and governed, and understanding what is fintech digitalization means recognizing the full scope of that change. The global fintech market is projected to reach $324 billion in revenue by 2026 with a 25% compound annual growth rate. For business professionals, entrepreneurs, and technology teams, that number signals one thing clearly: the organizations that understand this shift early will hold significant structural advantages over those that treat it as a trend.

Key takeaways

| Point | Details |

|---|---|

| Fintech is an ecosystem, not an app | Fintech digitalization spans payments, lending, AI, blockchain, and embedded finance, not just consumer apps. |

| Technology is the enabler, not the driver | Culture, leadership alignment, and governance determine whether fintech transformation actually succeeds. |

| Regulation is accelerating, not retreating | Frameworks like DORA, MiCA, and PSD3 are reshaping accountability standards across the entire fintech ecosystem. |

| Reverse integration outperforms acquisition | Banks that adopt fintech operating models, rather than absorbing fintechs entirely, retain the agility that makes those fintechs valuable. |

| Embedded finance is the next standard | Financial services integrated directly into non-financial platforms will define the next decade of consumer and enterprise experience. |

What is fintech digitalization: definition and scope

Fintech, at its core, describes the ecosystem of technology-driven innovation across financial services. It is not a product category. It is a transformation model that touches every layer of how money moves, how credit is assessed, how risk is managed, and how consumers interact with financial products.

The categories are wide. Breaking them down makes the scope concrete:

- Payments and transfers: Real-time payment rails, cross-border settlement networks, and digital wallets that process transactions in seconds rather than days.

- Lending and credit: Algorithmic underwriting platforms that assess creditworthiness using alternative data signals like behavioral patterns and cash flow history.

- Blockchain and digital assets: Distributed ledger systems enabling programmable money, tokenized securities, and transparent audit trails without central intermediaries.

- Neobanks and challenger banks: Fully digital banking institutions operating without legacy infrastructure, capable of releasing product updates on a weekly cycle.

- AI-driven financial services: Machine learning systems embedded across fraud detection, compliance monitoring, customer service, and investment management.

- Embedded finance: Financial products (insurance, lending, payments) delivered natively within non-financial platforms, from ride-sharing apps to e-commerce checkouts.

The structural difference between traditional finance and fintech-native systems is architectural. Legacy financial institutions were built around monolithic core banking platforms with update cycles measured in quarters. Fintech companies treat their technology stack as a product itself, modular and continuously deployable. That difference in design philosophy is what makes fintech digitalization a genuine transformation rather than an upgrade.

| Dimension | Traditional finance | Fintech-native model |

|---|---|---|

| Product release cycle | Every 4 to 6 months | Every 2 to 4 weeks |

| Infrastructure model | Monolithic core systems | Modular, API-first architecture |

| Customer data approach | Siloed by product line | Unified and accessible via APIs |

| Regulatory posture | Reactive compliance | Governance embedded in architecture |

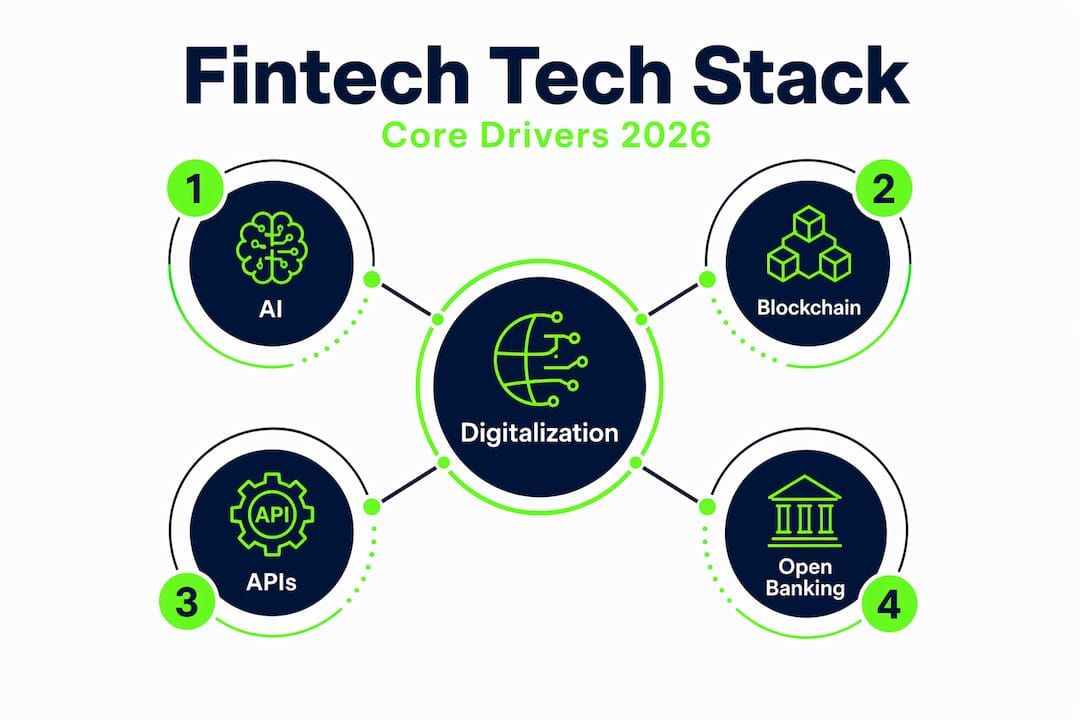

Core technologies driving the transformation

Understanding how fintech is changing finance requires looking at the specific technologies reshaping day-to-day financial operations. Four of them carry most of the structural weight.

Artificial intelligence is now embedded throughout the financial services stack. AI powers fraud detection, credit decisioning, and compliance surveillance at institutions that range from global banks to early-stage lenders. A credit decision that once required a loan officer review and a 48-hour turnaround now completes in seconds, with the model evaluating hundreds of data variables simultaneously. For a more detailed view of where AI creates the most measurable business value, AI applications in enterprise finance covers the specifics across multiple use cases.

Blockchain adds something traditional databases cannot: immutable, verifiable records without requiring a central trusted party. In payments, this translates to cross-border settlement that bypasses correspondent banking networks. In capital markets, tokenization of real-world assets like real estate or private equity allows fractional ownership and faster settlement. The transparency this creates matters for audit trails in regulated industries.

APIs and open banking form the connective tissue that makes the fintech ecosystem function. Brazil’s open banking program reached 60 million active consents and 100 billion API calls monthly by 2024, demonstrating how data-sharing infrastructure unlocks entirely new product categories. When consumers can authorize a third-party app to read their transaction history and initiate payments on their behalf, the competitive dynamics of financial services change completely. Incumbent banks no longer own the customer relationship by default.

Pro Tip: If your organization is evaluating open banking integration, start with read-only data access before building payment initiation. It dramatically reduces your regulatory exposure while you build internal capability.

The cumulative impact of these technologies on operational metrics is substantial. Speed improves because automated pipelines replace manual review queues. Cost decreases because software scales differently than headcount. Access expands because algorithmic systems do not carry the geographic and demographic biases that historically shaped credit availability.

Governance, risk, and regulation in fintech ecosystems

The most underestimated dimension of fintech digitalization is governance. Organizations that focus exclusively on the technology layer and treat governance as a secondary concern are building on unstable ground.

The risks in a fintech ecosystem distribute differently than in a traditional bank. When a bank integrates a third-party lending platform, a payments processor, and an AI underwriting model, accountability fragments across multiple parties. Governance failures and ecosystem risk redistribution increase institutional vulnerabilities in ways that do not always appear on a risk register until something goes wrong. The Wirecard collapse is a studied case of exactly this pattern: the technology worked, but the governance architecture allowed fraud to persist undetected for years.

Regulatory frameworks are converging to close those gaps. The key frameworks shaping fintech operations in 2026 are:

- DORA (Digital Operational Resilience Act): Requires financial entities in the EU to demonstrate resilience across their entire digital supply chain, including third-party technology providers.

- MiCA (Markets in Crypto-Assets Regulation): Establishes licensing and disclosure requirements for crypto-asset service providers operating in the EU.

- PSD3: The successor to PSD2, extending open banking obligations and strengthening consumer protection in digital payments.

- EU AI Act: Classifies AI systems by risk level and mandates specific governance controls for high-risk applications, including credit scoring and fraud detection.

“Institutions must define non-delegable control points and evaluate all technology decisions against regulatory constraints, not just commercial ones.” — Fintech Governance, Redcliffe Training

Regulatory frameworks are converging to address operational resilience, digital assets, payments, and AI simultaneously, which means siloed compliance teams can no longer manage these obligations in isolation. Integrated governance, where architecture and compliance design happens in parallel, is now the operational standard for institutions serious about long-term viability.

Pro Tip: Build governance control points into your system architecture from the start. Retrofitting compliance into a live fintech system costs three to five times more than designing for it upfront.

For teams looking to assess their current exposure, reviewing fintech security best practices alongside regulatory requirements provides a practical starting framework.

Business implications and competitive strategy

The impact of fintech digitalization on financial institutions is not theoretical. It shows up in product velocity, operational cost, and customer retention metrics. Traditional banks release new features every four to six months; fintechs release every two to four weeks, and banks operate at roughly 40% lower productivity on digital product delivery. That gap is widening, not narrowing.

The strategic response many banks attempted first, acquiring fintechs outright, often failed to deliver the expected benefits. The issue is cultural and architectural. When a fintech gets absorbed into a legacy institution, the compliance overhead, procurement cycles, and organizational hierarchy that made the acquirer slow tend to transfer to the acquired company, eliminating the agility that made it valuable.

Reverse integration offers a more effective model. Instead of absorbing the fintech, the bank adopts the fintech’s operating model and technology stack, running it as a separate capability layer that interfaces with legacy systems through well-defined APIs. This approach preserves the speed and flexibility of fintech operations while gradually exposing legacy infrastructure to modernization pressure.

The barriers to this approach are almost never technical. Culture and leadership create more obstacles than technology in the majority of failed digital transformation programs. Executives who have spent careers managing risk through process controls rather than architectural design often struggle to sponsor programs that require trusting automated systems and distributed decision-making.

The organizations getting this right share several characteristics:

- Cross-functional teams that include compliance, technology, and business product owners from the beginning of any initiative.

- Leadership that has built literacy in both regulatory requirements and software architecture.

- A clear separation between systems of record and systems of engagement, with APIs governing how they communicate.

- Investment in automated financial transaction processing to reduce manual touchpoints and the errors they introduce.

For entrepreneurs building in this space, the competitive opportunity lies precisely in the gaps that incumbents struggle to fill: real-time decisioning, personalized financial products, and embedded experiences that meet customers where they already spend time.

Future trends and how to stay ahead

The next wave of fintech digitalization is already forming around embedded finance. Embedded financial services could generate £3,500 in cumulative consumer benefit per UK household over the next decade. The mechanism is straightforward: when insurance is offered at the point of a vehicle purchase, or when a small business owner can access a working capital advance directly inside their accounting software, the friction that historically suppressed financial product adoption disappears.

AI governance is becoming a separate discipline from AI deployment. Boards are now being asked to approve AI risk frameworks, not just technology budgets. The EU AI Act makes explainability a legal requirement for high-risk use cases, which means the “black box” model that once satisfied a data science team now requires documentation that satisfies a regulator.

For professionals and entrepreneurs seeking to build capability in this space, emerging tech skill demand in 2026 points toward a convergence of API development, cloud-native architecture, and financial domain expertise as the most valued combination. Technical fluency alone is no longer sufficient. The professionals who understand both the regulatory constraints and the architectural possibilities will drive the most consequential programs.

Pro Tip: When evaluating fintech technology partners, ask directly how they handle non-delegable control points and audit logging. Their answer tells you more about long-term partnership risk than any technical specification document.

The organizations that will lead the next phase of digital finance are not necessarily the ones with the largest technology budgets. They are the ones that have built governance-first architectures, developed cross-functional leadership, and treated fintech digitalization as an organizational capability rather than a series of technology projects.

My perspective on fintech digitalization

I’ve worked closely enough with fintech transformation programs to say with confidence that most of the failures I’ve observed had nothing to do with the technology itself. The stack was adequate. The APIs were functional. The AI models performed within acceptable parameters. What broke down was always organizational: a compliance team that wasn’t consulted during architecture design, a leadership team that approved a vendor without understanding where accountability sat, or a culture that treated “digital transformation” as a project with an end date rather than a permanent operating mode.

What I’ve learned is that the institutions making real progress share one quality: they treat governance as an architectural input, not an afterthought. They define who owns each control point before the system is built, not after the regulator asks. That discipline is harder than it sounds because it requires the people responsible for risk management to have genuine influence over technical design decisions, and in most organizations those two groups barely speak the same professional language.

My honest recommendation for any professional navigating this space: before you evaluate a single vendor or approve a single technology investment, build a cross-functional map of who owns accountability at every layer of your fintech ecosystem. That map will expose more risk and more opportunity than any product demo.

— Bitecode

Build your fintech stack faster with Bitecode

Understanding the scope of fintech transformation is one thing. Actually building the systems that power it is where most organizations lose time and budget.

Bitecode’s modular development platform is purpose-built for exactly this kind of work. The AI Assistant Module automates financial workflows and customer interactions without requiring months of custom development. The blockchain payment system gives teams a production-ready foundation for secure, transparent transaction processing. With up to 60% of the baseline system pre-built, organizations can move from concept to deployment in weeks rather than quarters. For teams serious about digital transformation value for CFOs, Bitecode provides the modular foundation that makes it real.

FAQ

What is fintech digitalization in simple terms?

Fintech digitalization is the process of using technology to fundamentally change how financial services are built, delivered, and managed. It encompasses AI, blockchain, APIs, open banking, and embedded finance, not just digital payments.

How is fintech different from traditional banking?

Fintechs operate on modular, API-first architectures that release product updates every two to four weeks, compared to traditional banks that update systems every four to six months, resulting in significantly faster product innovation and lower operational costs.

What are the main benefits of fintech digitalization?

The core benefits include faster transaction processing, reduced operational costs, broader access to financial products, improved fraud detection through AI, and personalized customer experiences through data-driven systems.

What regulations govern fintech in 2026?

Key frameworks include DORA for operational resilience, MiCA for crypto-assets, PSD3 for digital payments, and the EU AI Act for high-risk AI systems. These apply accountability requirements across the full technology supply chain, including third-party providers.

Why do fintech transformation programs fail?

Most failures trace back to culture and governance gaps rather than technology shortcomings. Leadership misalignment, fragmented accountability across multi-party ecosystems, and compliance teams excluded from architectural design are the most common root causes.