TL;DR:

- Fintech teams often face manual, time-consuming processes like reconciliation and KYC that hinder operational efficiency. AI automation offers a practical solution by targeting high-frequency, rule-based workflows, with data quality and phased deployment as critical success factors. Successful implementation requires detailed process mapping, robust data infrastructure, and ongoing monitoring to ensure compliance and long-term performance.

Manual reconciliation runs at midnight. KYC reviews pile up faster than analysts can clear them. Compliance reports take days to compile from systems that don’t talk to each other. These are not edge cases in fintech operations. They are the norm. AI automation in fintech step by step is how forward-thinking finance teams are breaking out of this cycle. Deel’s AI platform saves over 91,000 hours monthly by automating workflows across finance, tax, and treasury. That number signals where the industry is heading. This guide gives you a practical roadmap to follow.

Key Takeaways

| Point | Details |

|---|---|

| Start with bounded workflows | Target high-frequency, rule-based processes like reconciliation or KYC before expanding to complex tasks. |

| Data quality determines outcomes | Audit and standardize your financial data before deploying any AI agent or automation layer. |

| Build in phases, not all at once | Phased deployment reduces risk and lets you validate performance before enterprise-wide rollout. |

| Monitoring is not optional | Implement audit trails and human oversight from day one to stay compliant and catch errors early. |

| Capture analyst expertise | Convert your team’s decision logic into automation playbooks to improve accuracy cycle by cycle. |

How to identify workflows ready for AI automation

The first and most consequential decision in any fintech automation initiative is not which AI model to use. It is which process to start with. Get this wrong and you spend six months automating something that delivers marginal value. Get it right and you build organizational confidence while generating measurable ROI from the first deployment.

The best candidates share a few characteristics. They are high-frequency, meaning they run daily or multiple times per week. They are rule-based or semi-structured, meaning a well-trained analyst follows a consistent logic to complete them. And they carry meaningful volume, where the manual effort compounds into significant person-hours per month.

Processes that consistently meet these criteria in fintech include:

- Payment reconciliation: Matching transaction records across multiple ledgers and payment rails, often involving thousands of records per batch

- KYC and AML screening: Document validation, watchlist checks, and risk scoring against defined rule sets

- Transaction monitoring: Flagging anomalies or threshold breaches in real time against compliance parameters

- Month-end close tasks: Journal entry preparation, variance analysis, and intercompany reconciliation

- Regulatory reporting: Aggregating data from multiple sources into structured report formats

Beyond process type, evaluate each candidate against four dimensions: manual effort in hours per cycle, data availability and structure, regulatory sensitivity, and failure cost if the automation produces an error. Reconciliation automation is a strong starting point because AI agents can autonomously investigate and resolve exceptions across financial asset classes, cutting manual workload without touching customer-facing operations.

Pro Tip: Map your top five manual workflows by time-per-cycle before selecting your automation target. The process your team complains about most is often your highest-ROI starting point.

Preparing your data and technical infrastructure

You can have the most capable AI model available and still get unreliable results if the underlying data is fragmented, inconsistently labeled, or incomplete. Data quality is the primary bottleneck in most fintech automation projects. Teams that skip the data preparation phase discover this the hard way, typically after a failed pilot.

Fintech organizations work with a mix of structured data (transaction records, ledger entries, account master data) and unstructured data (scanned documents, contracts, email correspondence, PDF statements). Both types need attention before automation can run reliably.

Start with a data audit that answers the following:

- Are transaction records consistently formatted across all source systems?

- Do legacy systems export data in machine-readable formats, or only as PDFs and flat files?

- Are there duplicate records, missing fields, or inconsistent identifiers across databases?

- Is historical data sufficient in volume and quality to train or configure the AI model?

“Poor data leads to unreliable automation.” This is not a caveat. It is a ceiling. The performance of any AI agent in a fintech workflow is bounded by the quality of data it ingests.

On the infrastructure side, you need to assess your integration architecture. Many fintech organizations operate a combination of modern cloud platforms and legacy core banking systems. Layered API architectures allow AI agents to connect with both without requiring a full system replacement. Where direct API access is unavailable, middleware layers and robotic process automation connectors can bridge the gap at lower cost.

Security and compliance infrastructure must be in place before deployment, not added afterward. This means encrypted data transit, role-based access controls, and audit-logging capability at the system level.

Pro Tip: Build a data readiness scorecard before committing to a deployment timeline. Score each source system on format consistency, completeness, and API accessibility. Any system scoring below threshold becomes a prerequisite task, not an afterthought.

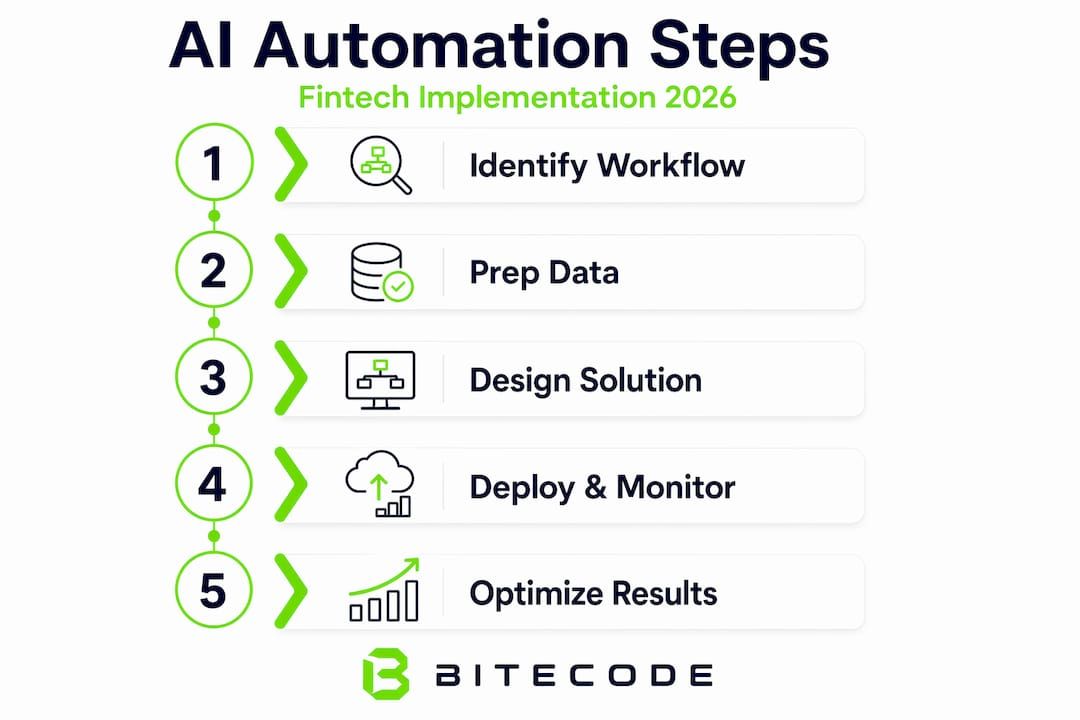

Designing, building, and deploying AI automation

This is where the fintech automation guide moves from preparation to execution. A structured eight-step approach covering task definition through deployment is what separates reliable AI agent implementations from pilots that never scale.

- Define the objective precisely. Specify what the agent must accomplish, what inputs it will receive, what outputs it must produce, and what constitutes a successful outcome. Vague objectives produce vague automation.

- Select your AI model and tooling. For document-heavy workflows like KYC, large language models with document understanding capability are appropriate. For numerical reconciliation tasks, deterministic rule engines combined with anomaly detection models often outperform generative approaches.

- Design a modular agent architecture. Separate planning, execution, and verification into distinct agent roles. This modularity makes the system easier to debug, audit, and extend. Multi-agent orchestration is particularly effective for complex financial tasks where one agent gathers data, another applies business rules, and a third validates outputs.

- Build workflow logic and automation playbooks. Translate your analysts’ decision-making process into structured logic trees and exception-handling rules. Institutional knowledge codified into playbooks is the foundation for continuous improvement across automation cycles.

- Implement compliance guardrails. Define hard limits the agent cannot override. For AML workflows, this means mandatory escalation to a human reviewer above certain risk thresholds. Compliance automation functions reliably when AI handles document understanding and real-time monitoring while humans retain final authority on high-risk decisions.

- Run a controlled pilot. Deploy the agent against a representative sample of live data, with humans running the same process in parallel. Compare outputs, measure error rates, and identify gaps in the workflow logic.

- Iterate before expanding. Do not scale until the pilot demonstrates consistent accuracy above your defined threshold. Gradual scaling following validated pilot results prevents the costly failures that come from premature enterprise-wide rollout.

- Deploy with governance in place. Establish who owns the automation, how exceptions are escalated, how the model is retrained or updated, and how performance is reported to leadership.

| Stage | Key action | Success indicator |

|---|---|---|

| Design | Define objectives and data inputs | Clear specification document signed off |

| Build | Develop agent logic and playbooks | Workflow logic reviewed by domain expert |

| Pilot | Run parallel with manual process | Error rate below defined threshold |

| Deploy | Activate with monitoring and governance | Audit trail active, escalation path tested |

Pro Tip: Involve your compliance and risk teams in the design phase, not the review phase. Their input on guardrail logic will save you significant rework after deployment.

Monitoring and optimizing automation over time

Deployment is not the finish line. AI automation in financial services requires continuous verification to remain accurate and compliant as regulations change, transaction patterns shift, and edge cases surface.

Systems that log all agent actions with explainability meet regulatory expectations and give operations teams the visibility they need to catch anomalies before they become incidents. Build monitoring dashboards that surface error rates, exception volumes, processing times, and escalation frequency in real time.

Meaningful KPIs for measuring automation effectiveness include:

- Cycle time reduction: Average time to complete a reconciliation run or KYC review before and after automation

- Error rate: Percentage of automated outputs requiring manual correction

- Exception escalation rate: How often the agent escalates to a human reviewer, and whether that rate is declining over time

- Cost per transaction: Total operational cost divided by transaction volume, tracked monthly

- Regulatory finding rate: Compliance breaches or near-misses attributed to automated workflows

Beyond metrics, build in a quarterly review process where your team validates automation logic against current regulatory requirements. AI-driven compliance workflows must be updated when KYC or AML rule sets change, not left running on outdated parameters.

Scaling successful automation to adjacent workflows follows the same preparation and pilot sequence. Do not skip steps because a previous deployment went well. Each new workflow carries its own data characteristics and edge cases.

Common mistakes that derail implementation

The most expensive mistake teams make is attempting to automate everything at once. Bounded, targeted automation consistently yields better ROI and faster organizational buy-in than sweeping transformation programs that take eighteen months to show results.

Other patterns that reliably cause implementation failures include:

- Deploying before data is ready. Rushed timelines create pressure to skip the data audit. The resulting automation produces inconsistent outputs, erodes trust, and is often abandoned before it can be fixed.

- Underestimating legacy system constraints. A legacy core banking platform may not expose usable APIs, requiring additional middleware development that delays deployment by weeks or months.

- Ignoring change management. Analysts who fear their roles are being replaced will find ways to work around automated systems. Early involvement, clear communication about role evolution, and visible leadership support make adoption measurably faster.

- Treating monitoring as a post-deployment task. Audit trails and alerting systems should be configured before the first automated run, not added after the first incident.

- Over-relying on vendor default models. Generic AI models not calibrated to your specific transaction data and business rules will generate false positives and negatives at rates that make them operationally impractical.

Pro Tip: Assign a dedicated automation owner for each deployed workflow. This person is responsible for monitoring metrics, managing exceptions, and coordinating retraining. Automation without ownership degrades silently.

You can find a deeper breakdown of measurable outcomes in Bitecode’s analysis of finance automation ROI strategies.

My perspective on where fintech teams go wrong

I’ve worked with enough fintech organizations on AI automation initiatives to recognize a pattern. The teams that struggle are not the ones with the worst technology. They are the ones that treat automation as a deployment problem rather than a knowledge-transfer problem.

The analyst who has spent three years managing reconciliation exceptions carries an enormous amount of decision logic in their head. Which counterparty codes signal a systemic break versus a one-off timing issue. When to escalate versus when to clear. What a false positive looks like for their specific asset class. That knowledge is worth far more than the model selection or the infrastructure choice. And most teams let it walk out the door untranslated.

In my experience, the organizations that achieve top fintech automation results spend more time on playbook development than on model selection. They sit with their analysts, map the decision trees, document the exception logic, and convert institutional knowledge into structured rules before writing a single line of automation code.

I’ve also learned to be candid about compliance complexity. Regulatory environments in fintech are not static. An automation that passes your internal audit in Q1 may need significant adjustment after a regulatory update in Q3. Teams that build transparent, auditable systems from the start absorb these changes without incident. Teams that deploy black-box processes find out about regulatory gaps from their examiners rather than their monitoring dashboards.

The future of fintech operations is not fully autonomous. It is a deliberate blend of AI agents handling volume and humans handling judgment. The organizations building that blend thoughtfully, with phased rollouts and genuine compliance infrastructure, are the ones positioning themselves for durable competitive advantage.

— Bitecode

Accelerate your fintech automation with Bitecode

For fintech teams ready to move from planning to execution, Bitecode’s modular platform removes the infrastructure burden that slows most implementations down.

The AI Assistant Module provides a configurable, enterprise-ready chat interface designed for workflow automation in financial operations. It connects to your existing systems without lengthy development cycles and includes the compliance logging and audit trail capabilities that regulated environments require. For organizations building or upgrading their payment infrastructure, Bitecode’s blockchain payment system delivers transparent, secure transaction processing that integrates directly with automated reconciliation workflows. Projects start with up to 60% of the baseline system pre-built, which means your team ships working automation faster and at significantly lower cost than greenfield development.

FAQ

What processes should fintech companies automate first?

Start with high-frequency, rule-based processes like payment reconciliation, KYC screening, and transaction monitoring. These workflows deliver measurable ROI quickly and build organizational confidence before you expand to more complex operations.

How long does it take to deploy AI automation in fintech?

A well-scoped pilot for a single workflow typically runs four to eight weeks from data preparation through initial deployment. Scaling to additional workflows depends on data readiness and the complexity of integration with legacy systems.

Why does data quality matter so much for fintech AI automation?

AI agents perform only as well as the data they ingest. Inconsistent formats, missing fields, and duplicate records produce unreliable outputs that require more manual correction than the original process. Data auditing is a prerequisite, not an optional step.

How do you maintain compliance in automated fintech workflows?

Implement audit trails that log every agent action with explainability, set hard escalation thresholds that route high-risk decisions to human reviewers, and schedule quarterly reviews of automation logic against current regulatory requirements.

What is the biggest mistake in fintech AI automation implementation?

Trying to automate too many processes simultaneously. Phased adoption focused on individual high-value workflows prevents the implementation failures and budget overruns that follow overambitious programs.